2025-04-24 22:06

publication

2025-04-24 22:06

Thursday session at New York stock exchanges brought strong increases in stock prices. Investors chose primarily the values of technological giants, and the S&PC index returned to the level of the day of the barrier to the “mutual duties” by President Trump.

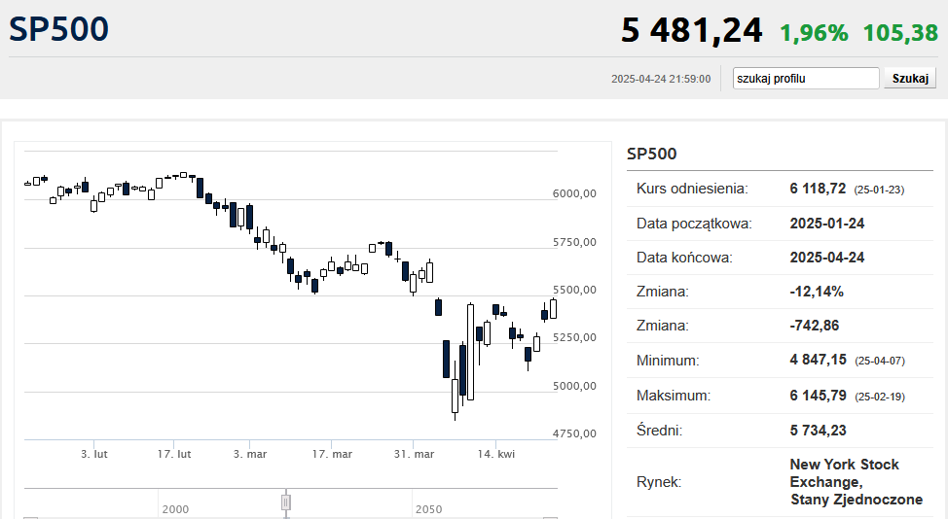

Dow Jones gained 1.23% on Thursday and checked in at the level of 40,093.40 points. The S&PLE increased by 2% and reached a height of 5,484.77 points. For the last time, this index was so highly equal to three weeks ago – on April 3, when President Trump caused a panic sale of shares after the announcement of the imposition of Dracon duties on almost all imports to the USA. It was the strictly media event of the White House host at the time called America's “day of liberation”.

But the real star of the day was Nasdaq, who gained 2.74% reached a height of 17,166.04 points. It is also the highest value of this index for three weeks. Nasdaq's increases have driven the growing ratings of large technology companies associated with the boom on AI. Nvidia, Microsoft and Amazon shares went up after about 3.5%, while the qualities of Broadcom and Palantir gained over 6%.

It is said that the pretext for purchasing was provided by a quarterly report associated with the Servicenow AI sector, whose shares gained over 15%.

We are now in the middle of the result season at Wall Street. So far, 157 companies included in the S & P500 index have shown reports for the first quarter. In 74% of cases, they managed to beat previously highly reduced analysts' estimates regarding the profit on action (EPS). Currently, the market consensus prepared by LSEG assumes that EPS has increased by 8.9%. So slightly more than 8% forecast at the beginning of April, but also clearly less than 12.3% assumed at the beginning of the year.

Procter & Gamble and Pepsico presented the results for balance, worse than expectations. These two companies and American Airlines have lowered or withdrew from year -round result forecasts, explaining increased uncertainty prevailing among consumers. P&G shares were overestimated by 3.7%, and the Pepsico rate dropped by almost 5%. Therefore, we see here the first “national” victims of the customs wars of President Trump and one of the lowest readings of consumer confidence meter in the USA in 70 years.

On the macroeconomic section we received a handful of tertiary indicators. The March orders for permanent goods, which increased by as much as 9.2% MDM (increased increases by only 2% MDM) were very positively surprised. But 1) These are extremely variable data from month to month and 2) we are talking about the lagoon for March ahead of the expected duties announced at the beginning of April. Anyway, without taking into account the means of transport, the value of orders remained the same as in February.

Nothing new was shown by weekly statistics of applications for unemployment benefit (222,000, compared to 216,000 a week earlier). These are still very low readings that the government performance department co -coined by Elon Musk is still too poor. The sale of houses on the secondary market in March scrubbed nearly 30-year minima and turned out to be lower than expectations. There was also a local industrial business index from Kansas, which fell to -5 points in April (z +1 points in March) under the line

KK