publication

2025-09-04 06:00

In the largest banks, the debit card is an absolute standard – virtually every customer uses it. PKO BP, Pekao, Santander, MBank and ING are the headlamp that distributes cards figuratively and literally. In smaller institutions and cooperative banks, many still choose cash. More and more people use mobile payments, but they are also based on the card.

The debit card is today the basic payment tool for Poles. It is issued for a regular personal account, i.e. ROR, and works in a very simple way: paying it in a store or internet, we spend funds that we already have on the invoice. There is no loan, debt or hidden limits – it's just a “extension” of our plastic account. Thanks to it, you can also withdraw cash from an ATM, check the balance or deposit money in the commercial. Although for many of us it is everyday life, it is worth recalling that for good debit cards they did not spread in Poland only in the 1990s – previously cash and check books dominated.

We have almost 37 million debit cards in their portfolios

At the end of the second quarter of 2025, there were about 36.6 million active debit cards in Poles' portfolios. This is a number that shows that almost every adult citizen has such a card – and some even a few. Compared to the beginning of the year, this is a slight growth, and in the annual scale, just over 1 percent came. cards. At the same time, the number of personal accounts reached 41.9 million. The increase in the number of RORs was only 2.4 percent. year on year. So it seems that the bank account market in Poland is approaching the saturation point. Almost every adult Pole already has them, and banks are fighting rather to “take over” customers from competition rather than completely new users.

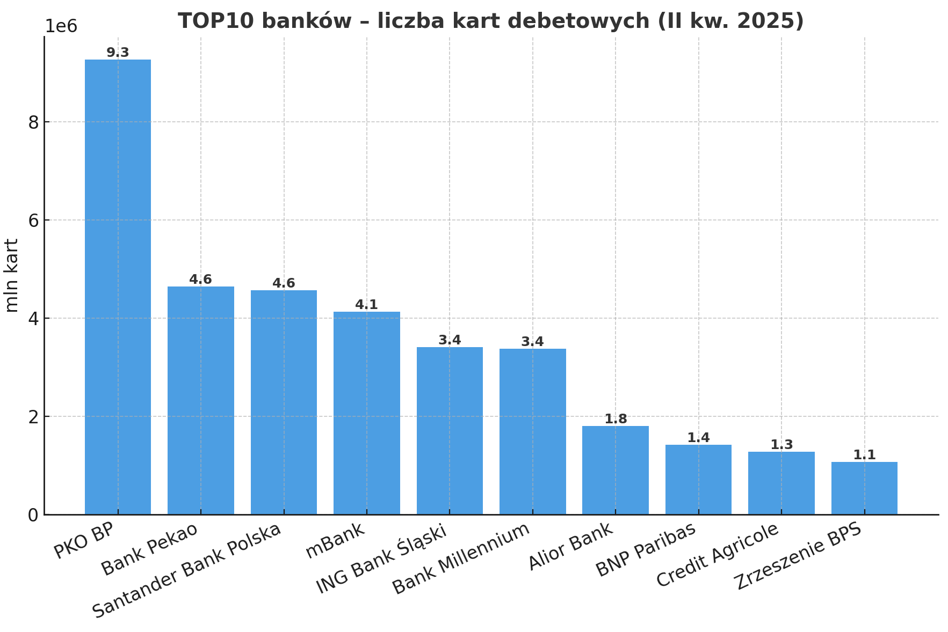

The debit card market remains heavily concentrated. The biggest player is PKO BP, whose cards make up about a quarter of all artists in circulation. Bank Pekao and Santander are still on the podium, followed by mBank and ING. Together, these five banks are responsible for over two -thirds of the entire market. This shows that in practice most of us use cards issued by the largest institutions. In smaller banks, the cards are also present, but their participation in the national scale is small.

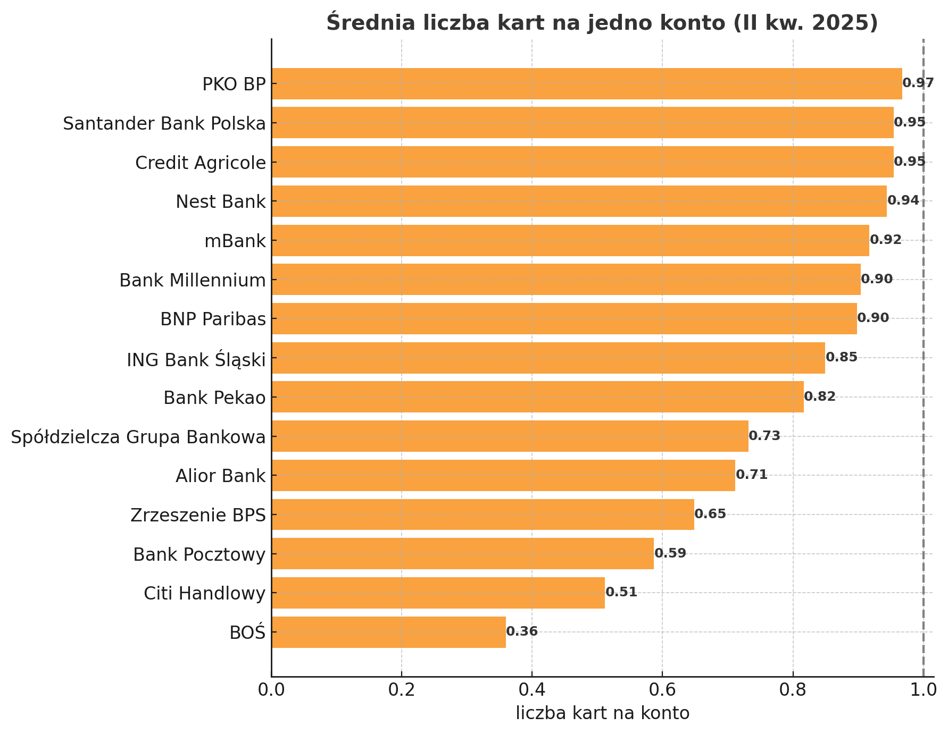

The relationship between the number of accounts and the number of cards looks interesting. In the largest banks – such as PKO BP, Santander or Credit Agricole – there is almost one card for one account. This means that virtually every account holder has plastic assigned. However, it should be remembered that these are some “virtual” calculations, because sometimes two cards are issued to one account, e.g. for spouses. In mBank or ING, this proportion is only a little lower, which shows that there a debit card is an integral part of the account. The situation in smaller institutions is completely different. On average, only every third account has a card, in Bank Pocztowy or Citi, just every second. In cooperative banks, there is also a clearly lower “chapter”. Perhaps this is due to the fact that some customers in smaller towns still prefer cash and do not need plastic for daily payments.

Mobile payments still need cards

In the debate on the future of cards, there is often a thread of mobile payments – a telephone, watch or band. It is worth remembering, however, that these gadgets are not an alternative to cards, but their extension. To be able to pay with a smartwatch or smartphone, you need to tie the device with a debit or credit card in advance. This card is a source of money, and the gadget only plays the role of a carrier. The exception is BLIK payments in the proximity version, which do not require plastic. This means that the debit cards will remain the foundation of the payment system for a long time, even if we use the phone more and more often instead of plastic.

After the second quarter of 2025, the debit card market in Poland is developing stable, but without spectacular jumps.

The largest players maintain a strong position, and smaller banks show that the customer's profile can significantly affect the popularity of cards. The number of accounts is only growing slowly, which confirms that we are dealing with a mature market. For banks, therefore, it becomes not the same challenge to acquire new customers, but to keep them and make them actively use the cards – whether in a traditional form or through mobile payments, which are still based on the card.