The year 2025 was marked by the “mortgage spring”. Heating competition between banks and falling interest rates have brought a series of favorable trends. Higher capacity, lower rates and a relaxed approach by lenders are the most important of them.

The year 2025 started rather sluggishly on the mortgage market. The first three months did not bring any visible changes in any of the areas important for potential borrowers. However, more serious changes soon came. In the second quarter, price movements finally began on the mortgage loan market, in the third quarter they gained momentum, and the end of the year is already a convergence of favorable trends.

Interest rate cuts played the first violin in shaping the market situation. Let us recall that the first reduction took place in May. Later, the Monetary Policy Council removed a “quarter” from the reference rate in July, September, October, November and December. In total, the reference rate dropped by 175 basis points, and with it the indicators determining mortgage interest rates.

Price descent in all its glory

In summarizing changes in the mortgage market, we refer to data from the monthly rankings of Bankier.pl. Over the last several months, banks have been preparing simulations for the same borrower profile. They are a couple with a child, living in Warsaw, taking out a loan for 25 years with a 20% down payment and a cross-selling package suggested by the bank. We have tracked a very similar type of customer before, which allows us to look at recent price trends from a further perspective.

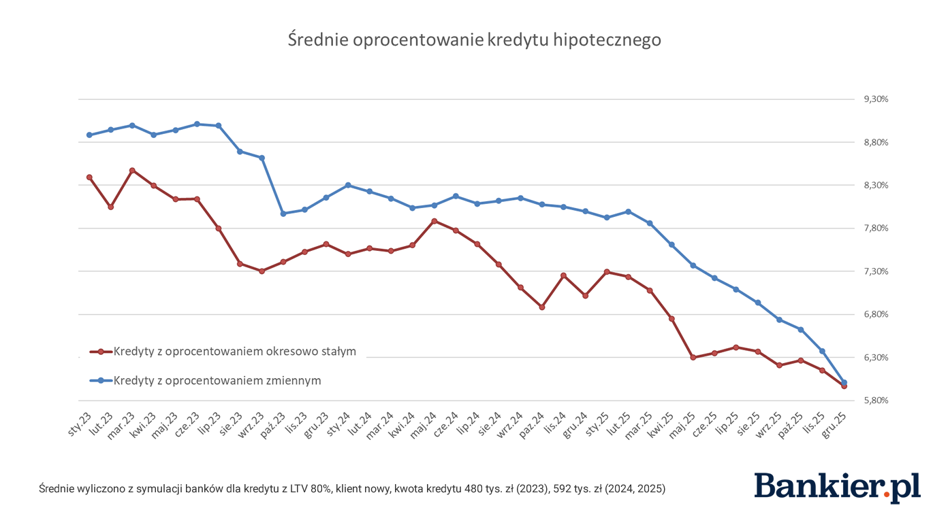

The interest rate on loans with a periodically fixed rate has broken through the symbolic “six” from below. In December, the average was at level 5.97 percent. In June, the average offer from banks was 6.35 percent, and at the end of the third quarter – 6.20 percent. The scale of the reductions can be seen when we make further comparisons. In January 2025, the indicator was nearly 7.3 percent, in January 2024 – 7.5 percent, and in January 2023 – 8.4 percent.

The end of the year brought another interesting phenomenon – the interest rates offered to customers for variable and fixed interest rates became much closer to each other. There is only a short distance between them. We may soon return to the times when we pay an additional premium for the guarantee of fixed installments compared to the initial conditions for a variable rate. This would be an understandable reaction to the end of the interest rate reduction cycle.

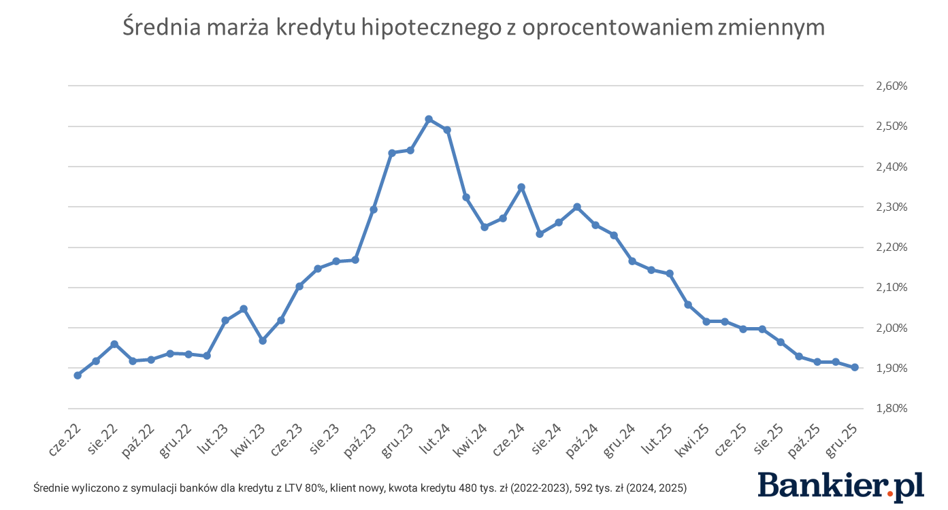

The average margin on variable-rate loans has returned from a really long journey. At the end of December 2025, it was almost exactly the same as three years earlier – 1.9 pp.

The chart shows two stages very clearly. The first one was marked by a rapid increase in margins, exceeding the level of 2.5 percentage points. at the end of 2023. Then a downward movement begins, which turned into a steady trend last fall. For borrowers interested in this formula, this meant that two favorable trends coincided. At the same time, margin rates and WIBOR rates, which are responsible for the second component of the interest rate, decreased.

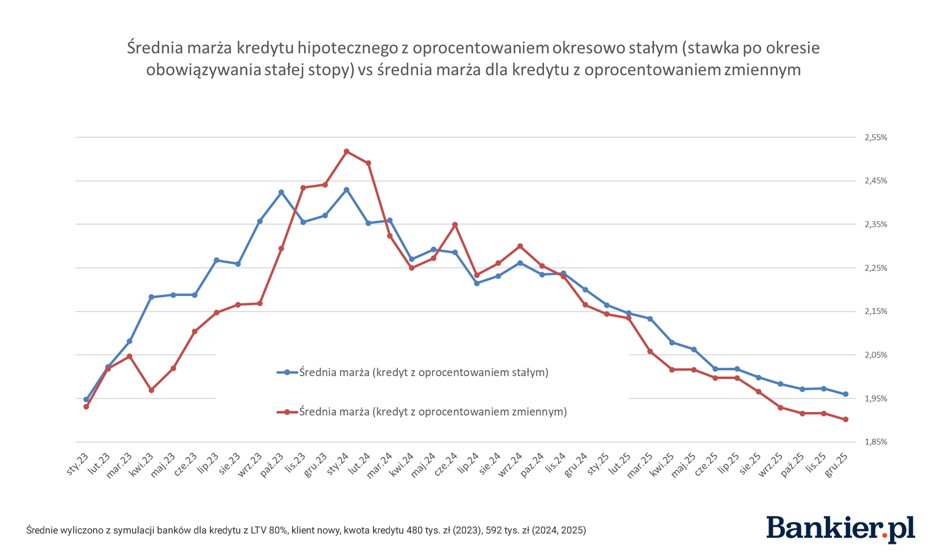

The new data also no longer shows any trace of the disturbing trend in bank price lists from about 2 years ago. Then, the margins for loans with a periodically fixed rate “diverged” from the margins for variable interest rates. We hypothesized that customers who chose a fixed installment for several years underestimated the margins applicable in the further period in comparisons, and banks took advantage of the opportunity to increase the price. The past year marked a return to normality. For both loan variants, the average margin has become closer to each other and, importantly, is falling. In December 2025 margins for fixed-interest loans were at the lowest level in the observed period (average 1.96 pp.).

Creditworthiness is breaking records

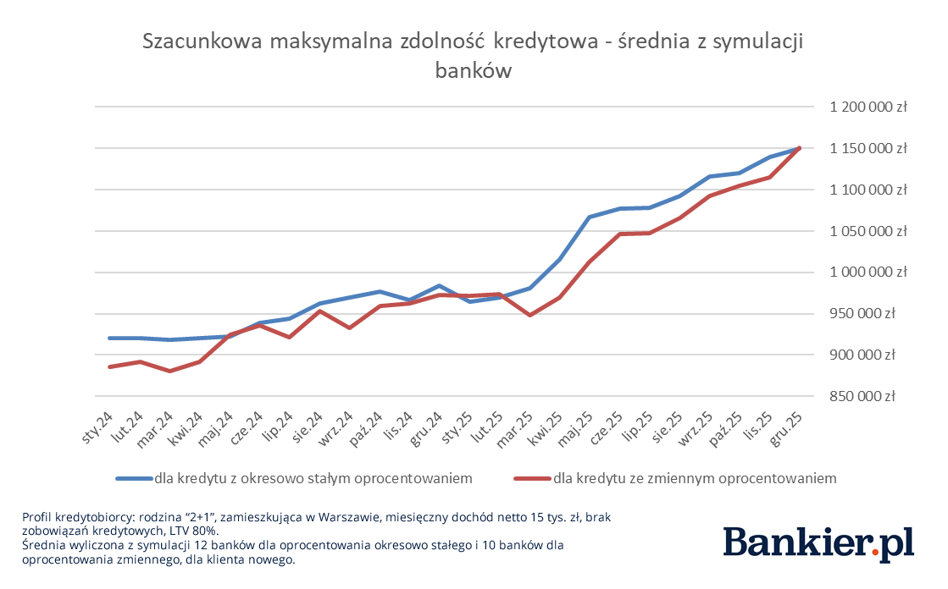

An example of a favorable long-term trend may be the constantly growing creditworthiness. The average of lenders' estimates in December once again broke previous records and reached PLN 1.15 million. The same family could count on PLN 964,000 in January. zloty.

The trend of increasing creditworthiness gained momentum when loan interest rates started to decline. Since May 2025, the lines on the chart have been climbing much faster, but we also see “convergence” here. This phenomenon has been observed since the beginning of the series of interest rate increases banks offering slightly higher amounts to borrowers who choose a fixed rate. We observed this effect in the rankings, although not in every month and not in every institution (sometimes, for example, a different product variant was responsible for the difference). December, however, brought almost equalization of the maximum estimated creditworthiness profile borrowers for both liability variants.

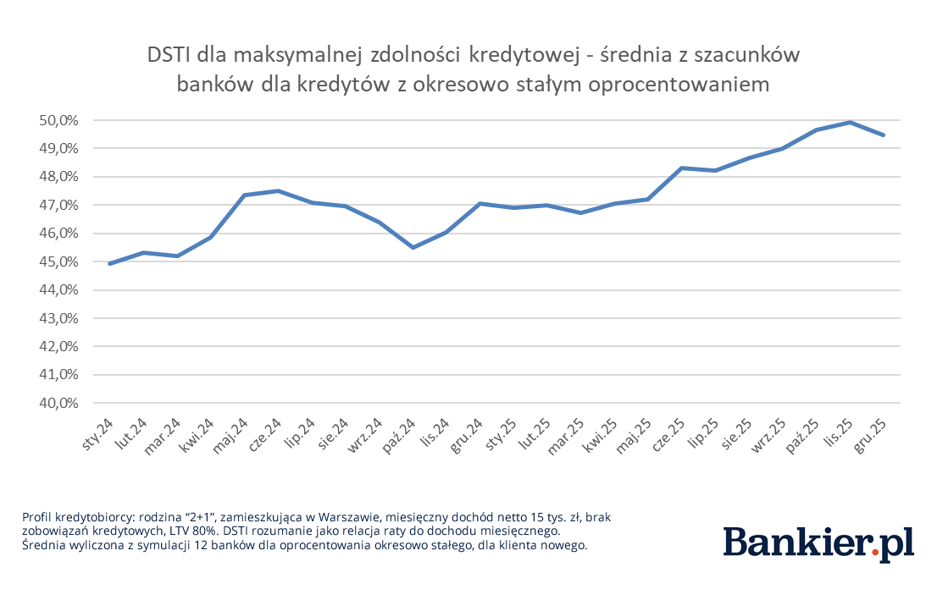

For each bank, in each month, we estimated the DSTI indicator resulting from the presented simulations. We recognize this indicator as the relationship between the installment amount for the maximum amount available to customers and the monthly household income (PLN 15,000).

The average of the DSTI indices increased slightly in the third quarter of 2025 to peak in November. Month-to-month changes are usually visible in the second decimal place, but in the longer term, it is impossible not to conclude that banks (on average) have loosened their approach. This is probably a factor that further enhances the upward march of creditworthiness.

What will the market be like when the “RPP engine” runs out?

There is a fairly common expectation that we are closer than further to the end of the interest rate reduction cycle. Therefore, the favorable trends in the mortgage market may soon slow down and we should forget about returning to the rates from 4 years ago. The 2 percent loan is now just a memory, unless we count the beneficiaries of the last subsidy program.

Nevertheless, 2026 may turn out to be a new chapter in the mortgage market. On the one hand, competition can be fueled by the competition to capture borrowers who are reaching the end of the 5-year repayment period and are ready to refinance their liabilities. However, this is not the only group that can benefit from loan transfer. Younger generations of borrowers also have this option, and the lack of early repayment fees in most banks means that the path to negotiations or “moving” is open.

Some hopes can also be associated with the entry of new players into the market and the awakening of institutions that are currently standing on the sidelines of the pitch. In this context, it is worth mentioning the debut of UniCredit as a lender and the prospect of Revolut's launch in mortgages. Let us also remind you that Bank Millennium and BNP Paribas Bank do not yet have a full offer of housing loans. Placing an emphasis on mortgages would probably help implement the strategic intentions of both institutions, which promise to fight for retail customers.

Although the era of “super-cheap” mortgage loans is not coming, we can at least hope that greater market movement will translate into better rates in price lists and faster procedures.