The European Central Bank did not reduce interest rates for the second meeting in a row. This is probably the final end of the cycle of monetary policy easing in the euro zone. Although in the case of central bankers you can never be sure of anything.

– The Governing Council decided today leave the three key ECB interest rates unchanged. Inflation is currently close to the medium-term target of 2% and the Governing Council's assessment of the inflation outlook has remained essentially unchanged, we read in the October statement of the European Central Bank.

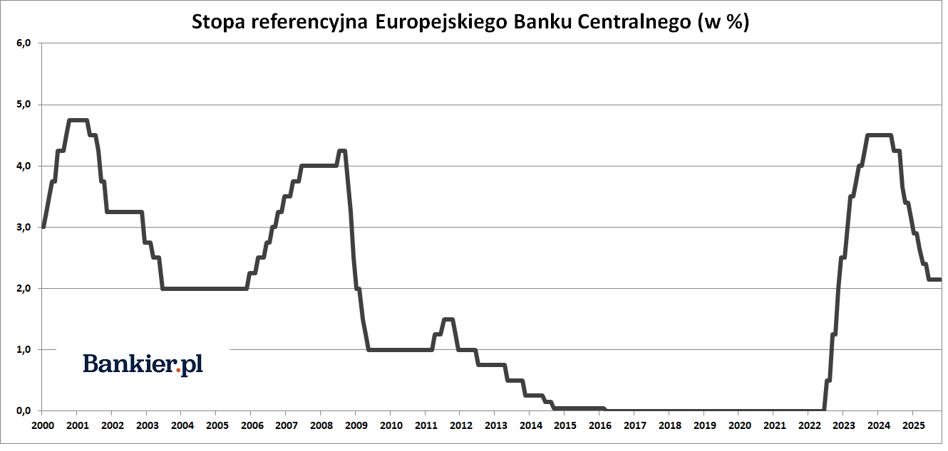

The deposit rate – which has been the key interest rate at the ECB for some time – remained unchanged at 2.00%. The rate of main refinancing operations was also not changed, which is 2.15%as well as the loan rate of 2.40%.

This was the third decision in a row to keep interest rates unchanged. The Governing Council delivered the same verdict in July as well as in September. The July decision was the first of its kind after eight cuts in a row as part of the monetary policy easing cycle that started in 2024.

How the ECB loosened its monetary policy

In June 2024, a decision was made to reduce interest rates in the euro zone for the first time since 2019. Previously, ECB rates were kept at the highest levels since 2001 for nine months. The total scale of these reductions amounted to 200 basis points. in the case of the deposit rate and 235 bps. in the case of the refinancing operation rate.

The previous reduction in borrowing costs at the ECB took place in June. Previously, the ECB cut rates at its meetings in April, March and at the end of January. In mid-December, the Governing Council also reduced borrowing costs by 25 basis points. In October, the ECB decided to cut rates by 25 basis points, and in September it also reduced the deposit rate by 25 basis points, while reducing the reference rate by as much as 60 basis points.

As a result, ECB rates have practically equaled HIPC inflation over the last 12 months. Preliminary Eurostat data show that the harmonized index of consumer prices (HICP) in the euro area in September 2025 was 2.2% higher than a year earlier. So this means resetting real interest rates in the Eurozone.

As part of the September inflation projection, ECB economists assumed that HICP inflation would average 2.1% in 2025, 1.7% in 2026 and 1.9% in 2027. Inflation excluding energy and food prices was predicted by experts to average 2.4% in 2025, 1.9% in 2026 and 1.8% in 2027.

The end of the cycle is probable, but not certain

The October decision of the Governing Council was not a surprise to economists and market participants. The former unanimously announced no changes in interest rates at the ECB. The last voices about a possible further reduction appeared in July.

– The Governing Council remains committed to ensuring that inflation stabilizes at the target level of 2% over the medium term. The Governing Council will determine the appropriate monetary policy stance on a data-driven basis, from meeting to meeting, as is customary, the ECB statement added.

The tone of recent statements by ECB President Crisitine Lagarde also spoke in favor of ending the cycle of interest rate cuts in the Eurozone. – The disinflation process in the euro zone has ended. What I mean here are the reasons for the increase in inflation that we have seen in recent quarters. We're still in a good place. Inflation is where we want it to be. The domestic economy is resilient, the labor market is in solid condition and the risk balance is more balanced, said the head of the ECB in September.

– However, this does not mean that monetary policy is on a predetermined path. We will make decisions from meeting to meeting, said President Lagarde as usual. She also added that a slight change in inflation from 2%. target will not immediately mean a reaction from the ECB.

However, Bank of America economists have a slightly different opinion on this matter. – Financial conditions have become significantly more restrictive. The ECB will have a problem avoiding their reflection in its December inflation forecasts, economists from the American bank believe. ECB chief economist Philip Lane also recently mentioned the risk of “undershooting” inflation, suggesting the option of a “slightly lower” interest rate. Hence, the futures market estimates the chances of another 25-point reduction in ECB rates by June 2026 at 40-50%.

Despite this, the vast majority of economists point to the risk of inflation exceeding the ECB's 2% target. They point to the recovery in the German service sector and the fiscal stimulus measures ordered by the government in Berlin that will soon come into force. Increased spending of borrowed money by the German government may raise both GDP and inflation in 2026.

European QT remains unchanged

In parallel to interest rate cuts, the ECB is pursuing a policy of “quantitative tightening” (QT) of monetary conditions. Under QT, the APP portfolio is reduced at a specific and predictable rate because the Eurosystem no longer reinvests capital repayments on maturing securities. As of July 2023, the Governing Council has stopped reinvestment under the APP program.

The APP and PEPP portfolios are being reduced at a specific and predictable pace as the Eurosystem is no longer reinvesting capital repayments on maturing securities, it said. The ECB stopped reinvestment under the PEPP program at the end of 2024.

The last of the planned decision-making meetings of the Governing Council in 2025 will be held on December 17-18