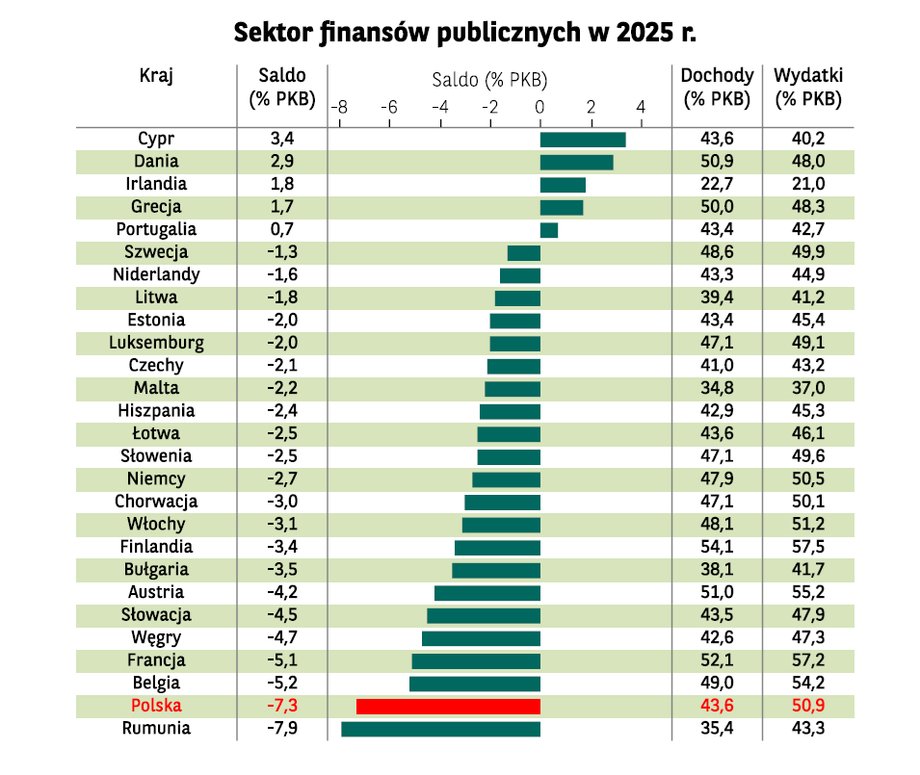

In the case of a deficit, this would mean only a slight decrease of 0.5 percentage points. with 7.3 percent GDP recorded in 2025 (almost PLN 284 billion), and this was unfortunately the second largest shortfall in the European Union countries (only Romania with an indicator of 7.9%) overtook us. The last time we recorded such a high deficit rate was in 2010 (7.4%), this result was even higher than the pandemic year of 2020, when funds to counteract COVID-19 were introduced. In the few years before the pandemic, this indicator was in check and reached from 2.6%. (in 2015) to 0.2 percent (in 2018).

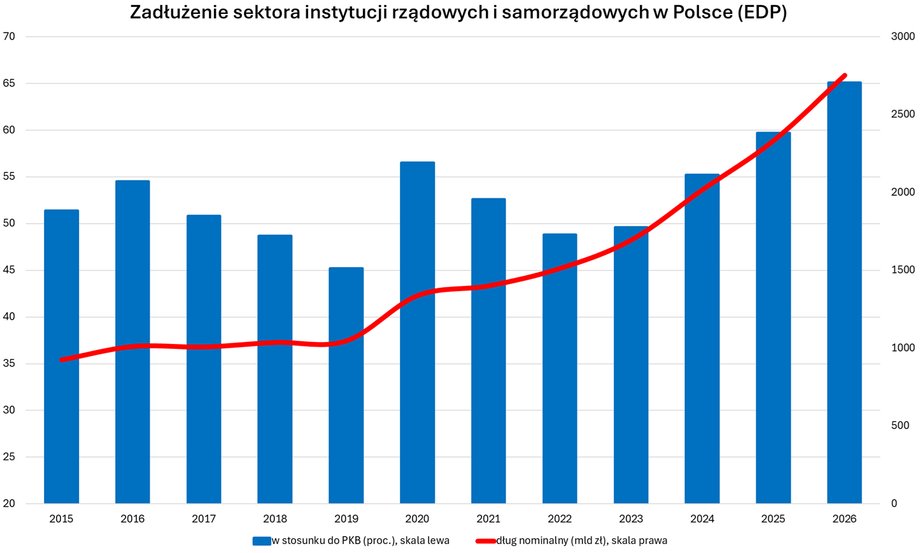

The debt of the general government sector amounted to PLN 2,335.1 billion at the end of 2025, i.e. 59.7%. GDP. We would like to remind you that this is EDP debt, i.e. compliant with the criteria of the Maastrich Treaty, it is a broader measure than PDP (state public debt, which does not include debt issued by Bank Gospodarstwa Krajowego, the Polish Development Fund or the Armed Forces Support Fund). This means that the debt to GDP ratio is expected to increase by 5.4 percentage points in 2026. and it would then be the highest in history. Recent years have seen a dynamic increase in this measure, at the end of 2019, i.e. in the last year before the pandemic, it was only 45%. In nominal terms, the debt may increase by approximately PLN 365 billion in 2026, to approximately PLN 2.7 trillion.

The public finance deficit increased significantly after the pandemic and the outbreak of the war in Ukraine.

|

Ministry of Finance, own study

While in the case of the deficit ratio we have been exceeding the limit provided for in the EU treaty (3% of GDP) for several years, in terms of debt to GDP we are entering completely unknown waters. We will exceed the 60% level for the first time in history. GDP, and this is one of the Maastricht criteria.

Compliance with requirements only thanks to technical measures

At the same time, this would mean exceeding the constitutional threshold of 60 percent, which would force the government to prepare a deficit-free budget for the next year. At the same time, it would also exceed the 55% threshold. from the Public Finance Act, which would mean the need to reduce the indicator in the next year, including freezing wages in the budget and indexation of social benefits.

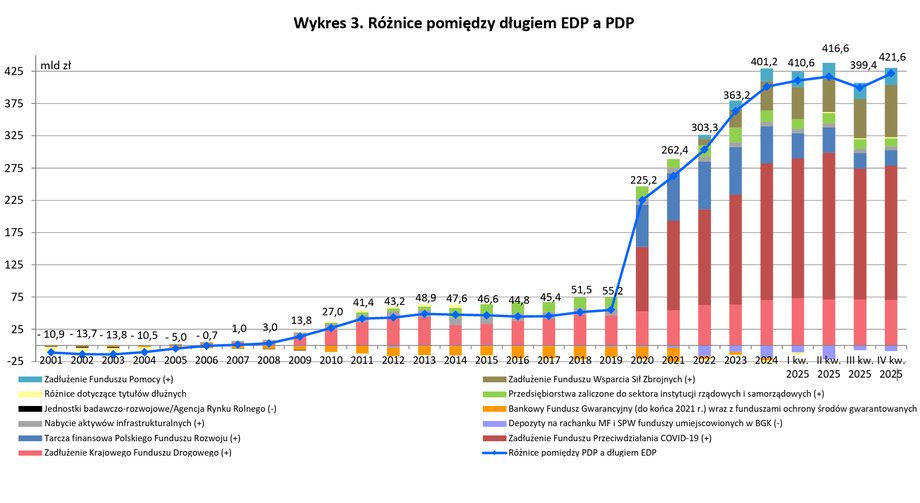

However, here is a very important caveat: the EU criterion concerns a broader measure of debt, i.e. EDP, but our national thresholds refer to PDP, and in this respect our debt measure is much lower (49.1% of GDP at the end of 2025). Of course, this is not a coincidence: governments consciously “push” spending outside the central budget to make more room for debt warning thresholds. As a result, the difference between EDP and PDP is growing and currently amounts to approximately PLN 422 billion, which is nearly 11%. GDP (before the pandemic, the difference between EDP and PDP was only PLN 50 billion).

The difference between the PDP and EDP debt increased dramatically in 2020, when pandemic prevention funds excluded from the central budget were created.

|

Ministry of Finance

— Exceeding the 60 percent threshold. GDP by sector debt general government is an important event, but this threshold is treated indicatively by the European Commission, and most EU countries have a debt exceeding this limit – comments Urszula Kryńska, head of the analysis and forecasts team at PKO BP.

See also: “Swedish welfare and Irish taxes”. Poland in the grip of social spending

Already in July 2024, the EU Council initiated the excessive deficit procedure against Poland due to its budget deficit, which in 2023 amounted to 5.1%. The EU controls the state of public finances of member states by determining the acceptable rate of expenditure growth. However, due to the need to incur increased expenditure on defense, these rules have been loosened. In January 2025, the EU Council recommended that Poland eliminate its excessive deficit by 2028 and that the nominal growth rate of net expenditure should not exceed 6.3%. in 2025, 4.4 percent in 2026, 4.0 percent in 2027 and 3.5 percent in 2028

— In the years 2024-2026, the growth rate of net expenditure will exceed the recommendations of the EU Council, which indicated that in 2026 the increase in expenditure should amount to 24.9%. compared to the level in 2023. Taking into account the Ministry of Finance's forecasts for 2026, this increase will reach 27.2%. However, thanks to flexibility exit clausePoland will formally remain in compliance with EU fiscal rules. Defense spending, which is important for the exit clause, is estimated to have increased to 3.4% in 2025-2026. GDP vs. 2.9 percent GDP in 2024 – emphasizes Kryńska.

The debt of public finances in Poland has increased significantly. The records in nominal terms are not surprising, but the growth in relation to GDP should cause increased vigilance.

|

Ministry of Finance, own study

— The national exit clause and the defense clause, for now, give the Ministry of Finance even more fiscal space than needed. We do not expect the EC to push for faster fiscal consolidation in Poland, reassures Sebastian A. Roy, economist at Bank Pekao.

Marcin Kujawski from BNP Paribas estimates that unless expenditure is further pushed beyond the budget, Poland will most likely exceed 55%. GDP limit in 2027 – That would mean that in 2029 we may face a sharp tightening of fiscal policy, the side effect of which would probably be a significant slowdown in economic activity, says the economist.

Cuts or raises?

In recent years, the statement that we have Swedish social security and Irish taxes in Poland has been gaining popularity. In other words, public spending – mainly on extensive social programs – is high in relation to GDP, and tax revenues are too low. Although the Polish economy is growing at a good pace and according to the latest government forecasts, GDP will increase by approximately 3.6% this year. — which makes it easier to “grow out of debt” (improve debt-to-GDP ratios) — it will be difficult to count on such rapid growth in the coming years (a gradual slowdown in GDP growth is expected to 2.2% in 2030).

— The budgetary situation remains tight, but we do not expect any reduction in social spending. In the current political situation, it is hard to imagine tax increasesbecause they would most likely be vetoed by the President – says Urszula Kryńska.

— The trajectory of public debt in the coming quarters and years is concerning. However, we do not think that there will be a significant tightening of the belt in the next two years. This is supported by the political calendar and the parliamentary elections scheduled for next year. However, there is no room left to increase spending, which should have a cooling effect on the pre-election promises made by the parties, says Marcin Kujawski.

Poland fares poorly in terms of deficit to GDP. The reason is a structural problem: relatively low income and high expenditure in relation to GDP.

|

BNP Paribas Bank Polska

“Poland formally meets EU requirements, but the improvement of fiscal balance is postponed. The overall picture of public finances is not surprising. Until the elections, the policy of maximum use of available fiscal space will most likely be continued” wrote Bank Millennium economists.

BNP Paribas analysts indicated in the latest market report that – considering the parliamentary elections scheduled for autumn 2027 – they are skeptical about the prospects for reducing the sector's deficit (at least) in the horizon of the next two years. “Taking into account that it seems likely that next year's election campaign will focus, among others, on the topic of health care and the need to increase its financing, we believe that belt tightening will be politically difficult to carry out,” they wrote.

This is what the Ministry of Finance itself assumes. According to the forecast included in the “Debt Management Strategy” published in September 2025, the public finance sector deficit is expected to fluctuate around 6%. GDP up to and including 2028.

Economists from Citi Handlowy expressed a similar tone, drawing attention to the political aspect, in the latest monthly report. “The medium-term fiscal prospects do not change. The next budget, which will be prepared by the Ministry of Finance in the coming months, will be the budget for the election year. Even if it does not include new generous proposals, it is difficult to count on a tightening of fiscal policy in these conditions. For this reason, we assume that deficit declines this and next year will be relatively small and will result primarily from increases in nominal GDP and freezing of tax thresholds and possible non-indexing of expenditures.

— Freezing taxes and spending is enough to improve the fiscal situation. The government expects a slight decline in the deficit this year (to 6.8% of GDP), and the main sources of improvement in the balance are to be maintaining the parameters of the PIT tax scale (+0.28% of GDP), excise tax measures (+0.16% of GDP) and changes in the CIT tax (+0.16% of GDP), says a PKO BP expert.

— In the short term, the increase in social spending does not seem to be at risk. I also do not believe that there will be any significant tax increases this or next year, says Sebastian A. Roy, economist at Bank Pekao.

He adds that in the longer term, balancing public finances will, in principle, require actions on the revenue or expenditure side. – In terms of the primary deficit (i.e. excluding debt servicing costs), already in 2026 we will see consolidation (from 4.7% of GDP in 2025 to 4.1% of GDP in 2026), and this will be greater than in the nominal deficit – he points out.

We are deprived of our safety cushion

Another question is whether loose fiscal policy is a problem for the economy. Theoretically, excessive spending may lead to increased inflation and does not accelerate debt consolidation (which makes its financing costs high). An additional risk is the lack of room for a fiscal impulse in the event of a crisis.

“So far, the macroeconomic costs associated with the growing deficit have been practically unnoticeable thanks to the more restrained attitude of the private sector (households, enterprises), which significantly increased its savings and balanced the “prodigality” of the public sector. However, excessive spending can be a latecomer. They put Poland in a particularly vulnerable position in the event of a shock such as in 2008 (financial crisis) or 2020 (pandemic).” – said BNP Paribas economists.

They added that in the event of such an event, the space for the authorities to support the economic situation will be significantly limited. “The hole in public finances is currently – despite very solid economic growth – similar to that at the peak of previous crises. The lack of fiscal consolidation is therefore a very risky game which, in a worst-case scenario, may have severe consequences for the national economy.“- they added.

Author: Maciej Rudke, journalist of Business Insider Polska