The Federal Open Market Committee, in line with the expectations of investors and economists, decided not to change the level of interest rates. However, what is more important for the market is what the new FOMC macroeconomic projections showed – and especially the so-called fedecrops.

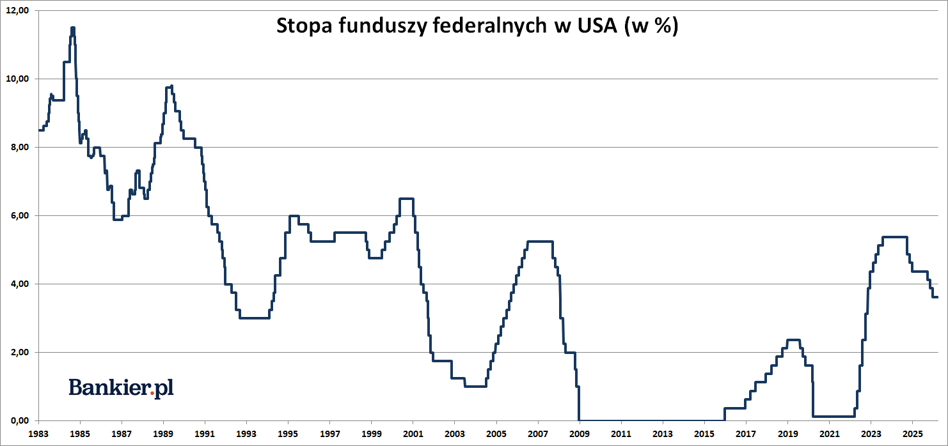

The federal funds rate range remained unchanged 3.50-3.75% – announced the Federal Open Market Committee (FOMC) in a statement. This is the second decision in a row to keep interest rates unchanged after three consecutive cuts (25 basis points each) made in the fall of 2025.

This decision did not raise any controversy on the market. The futures market estimated the chances of such a decision at almost 99%. Most economists also expected no cuts. It is worth noting that The FOMC's decision was again not unanimous. Stephen I. Miran was in favor of lowering interest rates demanded a 25-point reduction in loan costs.

In September, the FOMC bowed to pressure from the White House and decided to reduce borrowing costs by 25 percentage points after a nine-month break. Also at the October meeting, a decision was made to reduce the FFR by 25 points. And in December to another -25 bp. The FOMC also added the resumption of QE (i.e. quantitative monetary easing) amounting to USD 40 billion per month.

Before the March FOMC meeting, the futures market was pricing in the next increase in the federal funds rate for September at the earliest, giving this scenario less than a 50% chance. Even one 25-point cut will not be fully discounted by the end of the year, although a month ago the market was pricing in at least two such moves (including the first one in June).

Will the Fed wait and hold off on rate cuts?

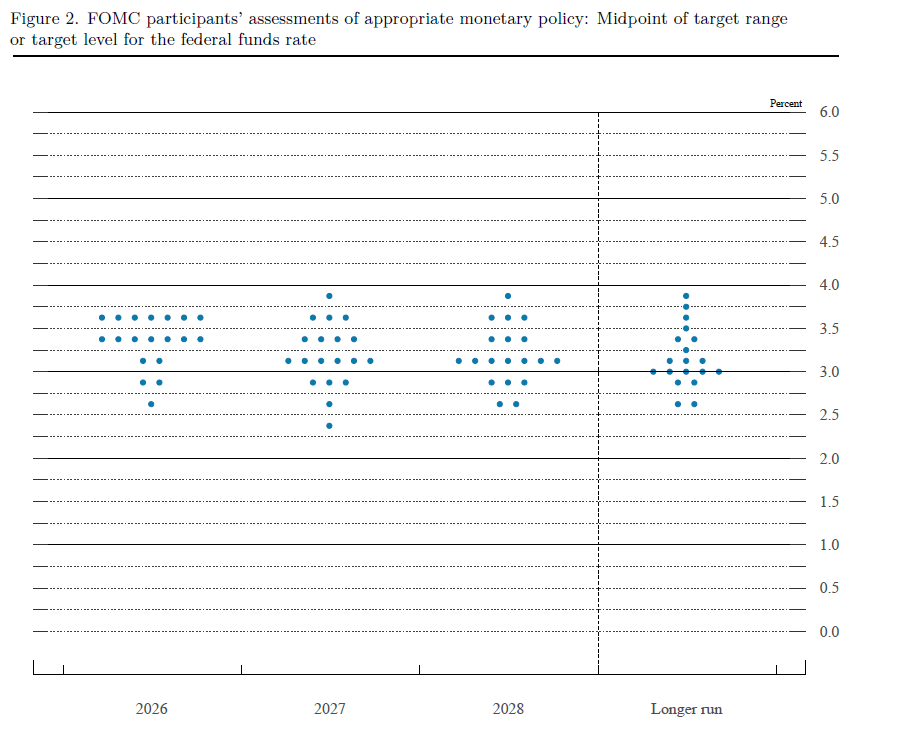

In December, the so-called fedokropki assumed that by the end of 2026 the federal funds rate range would be reduced by only 25 basis points. That is, by 25 bp. less than the quotations on the futures market indicated at that time. In this respect, everything has remained the same. There is still a majority within the FOMC ready to pass a single 25-point rate cut in 2026. And another one the following year.

– The Committee is strongly committed to supporting the full employment mandate and bringing inflation back to the 2 percent target – recalled the Federal Open Market Committee in a January statement. This is probably in case anyone has doubts about whether it is justified to lower interest rates when CPI inflation has been exceeding the Federal Reserve's 2% target for 5 years.

Advertisement

– Uncertainty regarding the economic outlook remains elevated. The consequences of developments in the Middle East for the US economy are uncertain. The Committee is sensitive to the risks for both sides of its dual mandate, we read in the March statement of the Federal Open Market Committee.

As usual, the FOMC reserves the right to change the stance of monetary policy, adapting it to the changing economic and financial reality.

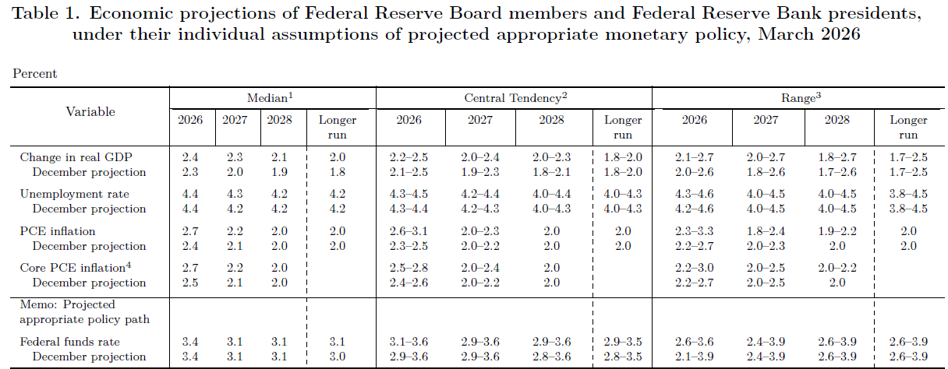

As every quarter, Committee members also updated their macroeconomic projections. Those in March differ quite significantly from those in December. GDP growth in 2027 (2.3% compared to 2.0% in the December projection) and in 2028 (2.1% instead of 1.9%) is perceived more optimistically. Next year's unemployment rate is expected to be slightly higher (4.3% instead of 4.2%).

The biggest difference is the core PCE inflation forecast for this year. Here, the median forecast increased to 2.7% compared to 2.5% in the December projection. In fact, with such expectations for future PCE inflation, there is not much room for any reductions in the federal funds rate.

Powell: If inflation doesn't come down, you won't see rate cuts

– The US economy is growing at a solid pace. Although employment growth is low, the unemployment rate remains low. Employment is stable and inflation remains slightly elevated. We remain attentive to both sides of our dual mandate – that's how Federal Reserve Chairman Jerome Powell began his March news conference.

Powell said that developments in the Middle East raise uncertainty for the prospects of the US economy, but he did not mention the quite obvious risk of rising inflation. He concluded that the current monetary policy stance is appropriate to “promote progress towards full employment and the 2% inflation target” (the latter has been exceeded for 5 years, editor's note). According to Powell, the current level of the federal funds rate is within the neutral monetary policy stance.

– We are aware of the inflation results over the last 5 years and it was the effect of external shocks (…) – this is how the head of the Fed replied to the question about the impact of the oil shock on the already elevated inflation. He added that the FOMC is now primarily looking at the impact of the tariffs introduced a year ago on the prices of industrial goods. In his opinion, customs duties are responsible for approximately 0.5-0.75 points. percent annual core PCE inflation.

– If we don't see progress on the inflation front, you won't see interest rate cuts – Jerome Powell pointed out.

– Nobody knows the scale of the costs of the oil crisis. If we have a longer period of higher fuel prices, this will affect disposable income and consumption. But we don't know if this will happen (…) Meanwhile, economic growth is solid and inflation is overshooting mainly due to tariffs, says the chairman of the Federal Reserve.

When asked directly about the credibility of maintaining a 2% inflation target, Jerome Powell excused himself with the fuel shock, the pandemic, tariffs and the war in Ukraine. He added that the most important thing for the FOMC is to maintain stable inflation expectations. Powell assured that the current excessive inflation comes mainly from the process of passing on tariffs to consumers, and not from the Fed's overly expansionary monetary policy.

The publication contains affiliate links.