On Thursday morning on the Warsaw Stock Exchange, the CCC price falls by approximately 9%. percent to PLN 116.9, with an increase in the WIG20 index by 0.7%. This is a reaction to preliminary results for the fourth quarter of fiscal year 2025, which it published late on Wednesday evening. The group announced that it expects EBITDA from PLN 180 to 220 million in the fourth quarter, and in the entire 2025 EBITDA result in the range of PLN 1.43 billion to 1.47 billion.

The company announced that it has verified the expected level of consolidated EBITDA in 2025 based on the actual performance of the first two months of the fourth quarter of the financial year and the estimate of financial results for January.

CCC indicates consumer weakness and weather

— The results are poor, we have a weak quarter. We were let down by sales, we had poor LFL in malls. However, the business model is becoming more mature and has scaled, said CEO Dariusz Miłek on a teleconference on Thursday morning. He added that e-commerce sales are a disappointment. LFL (like for like) is the year-to-year sales dynamics in stores operating for at least a year.

The main differences in relation to the current assumptions of the group's results in the fourth quarter are the lower level of sales revenues by approximately PLN 500 million (due to the lower than expected level of LFL sales (slightly negative) and lower sales dynamics in the e-commerce segment); gross margin lower by approximately 2 percentage points (due to greater promotional activity aimed at stimulating traffic); one-off events (including write-offs for defective goods, increase in write-offs for receivables and unfavorable impact of exchange rates) – impact on the result of approx. PLN 65 million.

— The level of revenue was certainly influenced by the consumer weakness that we observed this quarter, which primarily translated into lower traffic levels. In our stores, this traffic translated into LFL of minus 1.9%. in constant currencies, which – we believe – that with such a dynamic expansion and also against the background of the competition and the data coming to us from the market, the result is relatively decent, although certainly unsatisfactory – said the vice-president of CCC Łukasz Stelmach.

— When it comes to e-commerce revenues, we saw a 23% reduction. Largely as a result of deliberate actions related to the transformation of our e-commerce model towards higher profitability – he added.

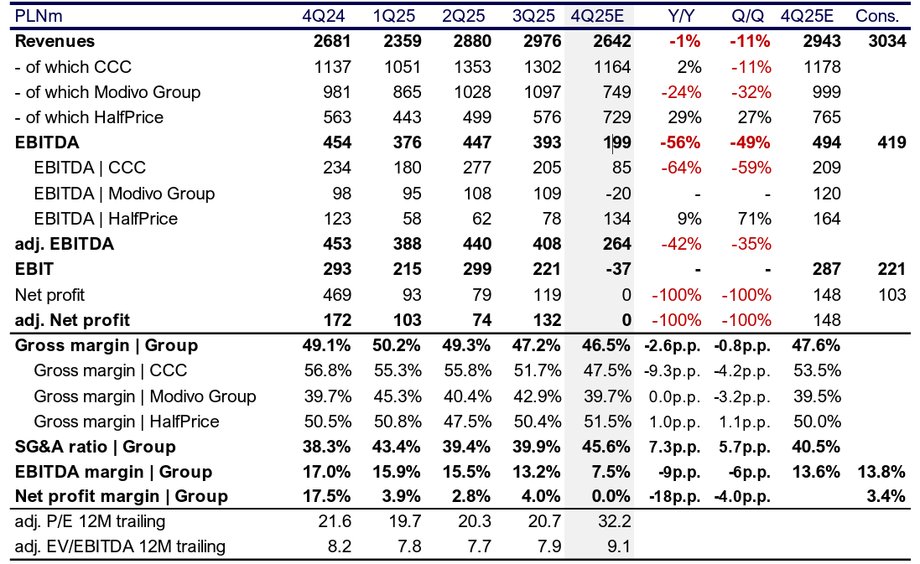

Consolidated results of CCC (PLN million, unless otherwise indicated).

|

Trigon DM

President Miłek assessed that the CCC results were under the pressure of unfavorable weather throughout the year. — Weather pressure, traffic pressure and our inventory meant that we invested a lot in the discount. We wanted to release a lot of goods. Now, in January, we sell winter well, but at large sales, said the president.

CCC expects 18% in the fourth quarter of 2025. EBITDA margin in the HalfPrice brand, 7 percent in CCC (of which 14% in CCC Omnichannel) and -2%. in the Modivo Group.

It was also indicated that due to the lower than planned level of sales and the acceleration of deliveries of the spring-summer collection, CCC expects a slightly higher than previously assumed level of group inventories at the end of 2025 (approx. PLN 3.7 billion – does not take into account the possible consolidation of MKRI).

CCC hopes to improve its results in 2026

CCC expects a higher gross margin in 2026, which is expected to result from better terms of purchasing the collection, a lower scale of discounts, and a higher share of licensed brands in sales.

The company assumes a lower cost ratio – mainly the effect of operational leverage (higher sales/m2 for stores opened before 2026 – the so-called maturation effect, lower share of newly opened stores in the total number of stores) and more cost-effective logistics for HalfPrice.

— We expect improved results this year, said CCC vice-president Łukasz Stelmach. As he pointed out, the improvement will be supported by, among others: retail space 28% higher at the beginning of the new financial year. y/y (including Worldbox franchise stores 36 percent) and the development of new retail space (an increase of approx. 25 percent).

CCC expects a higher gross margin in 2026, which is expected to result from better terms of purchase of the collection (delivery, exchange rates, freight), lower discounting scale, and higher share of licensed brands in sales.

The company assumes a lower cost ratio – mainly the effect of operational leverage (higher sales/m2 for stores opened before 2026 – the so-called maturation effect, lower share of newly opened stores in the total number of stores) and more cost-effective logistics for HalfPrice.

When asked whether the company maintains its previous assumptions for 2026, CCC representatives replied that the group does not currently have an official forecast.

— Internally, we have big ambitions, we want this year to be a breakthrough, but… we want to talk less and deliver more – said president Dariusz Miłek. — We will not say what our financial result will be, because we would need to know what LFL's sales will be. There is no reason for LFLs not to be positive, because in 2025 they were weak, he added.