In Business Insider Polska we present the second edition of the conclusions from the Lendi report (you can read the first part here), the full premiere of which is scheduled for January 14. This time, the authors of the study look at how young Poles finance the purchase of real estate and what raises the greatest concerns in this process.

Just a few years ago, developers' main clients were people in their thirties and forties – people with a stable professional situation, often buying larger apartments or houses, often also for investment purposes. Today, the demand structure is clearly shifting.

People under 35 years of age are increasingly driving the sale of apartments, especially in large cities. They buy their first apartment, smaller spaces, often with security and stability in mind, not as an investment. At the same time, this is it this group suffers the most from market entry barriers.

The Lendi report was based on a Morizon–Gratka study conducted in July 2025. The online survey covered over 1,000 people planning to buy an apartment. Respondents answered, among others: to questions about financing sources, stress level, use of online tools and the role of financial experts in the purchase process.

Mortgage loan is the biggest source of stress

Although high prices per square meter are still a challenge, the data from the report clearly show: it is financing the purchase of real estate that generates the greatest emotional tension.

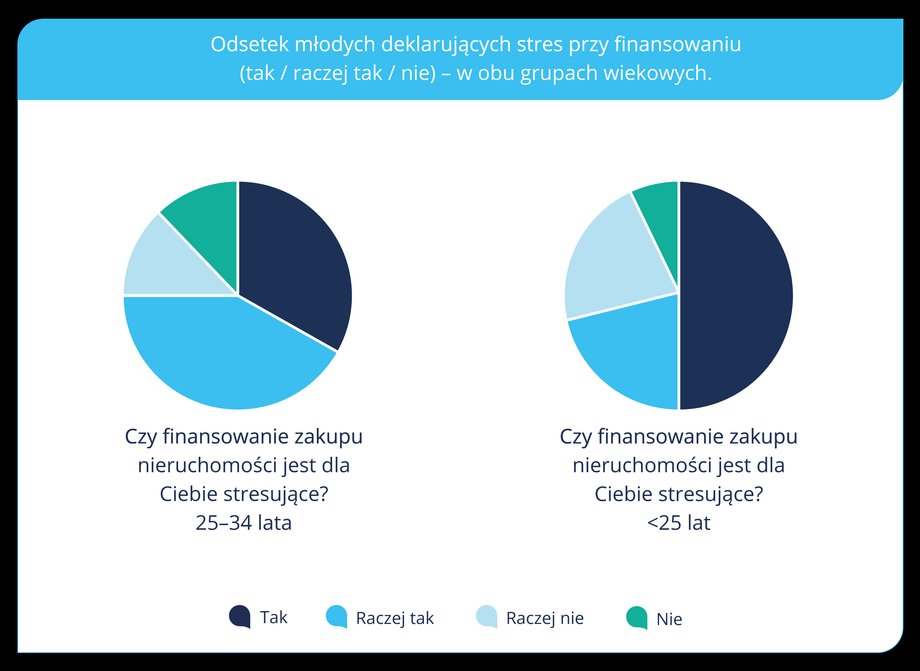

In the group of people under 25 years of age, as many as 71.4 percent respondents declare stress related to their mortgage loan. Importantly, almost half of them talk about severe stress that they experience on a daily basis. In the older group – 25-34 years old – this percentage is even higher and reaches 75%, although it is more often moderate (“rather yes”).

The above-mentioned chart shows the percentage of young people declaring stress when it comes to financing – with a clear division into the answers “yes”, “probably yes” and “no” in both age groups.

Two generations, two different credit fears

The Lendi report clearly shows that the sources of stress vary depending on age and life stage.

Financing stress

|

Lendi

Read also: Plot without a local plan? Find out how not to lose your right to build

People under 25 years old most often indicate:

- lack of professional experience,

- unstable or low income,

- uncertainty about creditworthiness,

- fear of rejection of a loan application.

For many of them, a mortgage loan appears to be an abstract, long-term obligation whose terms they do not fully understand.

In a group 25–34 years old the situation is different. Here they appear more often:

- more stable income and real creditworthiness,

- family obligations,

- concerns about the amount of the installment and its impact on everyday life,

- fear of changes in interest rates and the economic situation.

The market has real tools to reduce the stress levels of young buyers

|

Paula VV / Shutterstock

See also: Survey: uncertainty on the real estate market in 2026 caused by the war in Ukraine

Fear of a contract you don't understand

Many respondents admit that the biggest problem is not the installment itself, but the fear of signing a contract whose provisions they cannot fully understand. This feeling of lack of control increases stress and often leads to postponing decisions.

— The question I most often hear from young people is: what if I miss something and end up with a contract that I don't understand? This describes the essence of the problem well – stress is not only about money, but also the fear of making a mistake that will cost you your whole life – says Tomasz Pilecki from Lendi.

Similar observations come from the development market.

— We often see that young clients give up not because they can't afford it, but because they are afraid of the process. That's why we introduced it simple credit simulations and constant online supportto relieve them of some of this burden – admits the sales director of one of the development companies.

How can the real estate market reduce credit stress?

Although developers and intermediaries have no influence on banks' decisions, the Lendi report shows that the market has real tools to reduce the stress level of young buyers. The key are:

- transparent information – clear communication of the total purchase costs, including additional fees,

- decision support tools – installment calculators, creditworthiness simulations, step-by-step guides,

- predictable purchase process – clear stages, investment schedule, no “surprises”,

- easy access to a financial expert – quick consultation without having to look for information yourself.

Experts: Apartment prices are no longer the only barrier

— My research clearly shows that a mortgage loan is the greatest source of stress for young people today in the entire process of purchasing a flat. Over 70 percent people up to 35 years of age says directly that financing is a burden on them – emphasizes Tomasz Pilecki, Lendi.

— Young people start counting very early: they use calculators and compare offers. The problem is that these tools only provide orientation, and the lack of full understanding quickly turns into uncertainty and postponing decisions, he adds.

From the perspective of working with clients, Adam Janowski, a financial expert at Lendi, describes a similar situation.

— Most conversations today start with numbers: capacity, installment, range of possibilities. Only then do emotions appear – and very often it is stress. Customers are afraid of losing their deposit, changes in interest rates or the economic situation. “My role is to translate the numbers into an understandable plan and show what this decision means in everyday life,” he says.

Conclusions for the housing market

There are several key conclusions from the second part of the Lendi report:

- Credit stress is barrier No. 1 – over 70 percent experience it. young,

- the problem is not only money, but lack of knowledge and sense of control,

- simplifying communication and access to experts can actually unlock demand.

For young people today, a mortgage loan is not just a statistic, but an everyday reality. For the real estate market – the most serious challenge that must be overcome if the potential of the young generation is to translate into real purchasing decisions.