Inflation is the goal, but at the expense of interest on deposits. Summary of the deposit market in 2025

Readers who follow the situation on the deposit market will have no problem describing the past year in one word. The key word will be “reductions”, and it is no wonder, because in 2025 we touched on this topic many times in Bankier.pl. However, articles with extensive tables did not appear out of thin air – banks massively cut rates as a response to the reductions in interest rates of the National Bank of Poland.

And there was no shortage of them. This year, the Monetary Policy Council reduced the reference, lombard, deposit and rediscount rates six times. The first cut took place in May this year, then in July, September and subsequent months until the end of this year. Comparing the rates before the first cut and now, the difference is as much as 1.75 percentage points.

No wonder the interest rates on deposits and savings accounts were getting lower, although some banks maintained relatively high interest rates as a lure for new customers. An example is the leader of monthly rankings, i.e. Bank Nowy. The rate on the NOWYdepozyt 1M HIGH PERCENT deposit is 7%. per annum from January 5, 2024 and is the highest for this period.

The lowest rates in 3 years

|

The highest interest-bearing deposits for PLN 10,000 with additional conditions |

||||

|---|---|---|---|---|

|

Deposit period |

The percentage rate for a given period |

|||

|

December 2022 |

December 2023 |

December 2024 |

December 2025 |

|

|

1 month |

8.40% |

8.00% |

7.00% |

7.00% |

|

3 months |

8.30% |

7.00% |

7.50% |

7.00% |

|

6 months |

8.10% |

7.10% |

7.60% |

6.60% |

|

12 months |

8.20% |

6.50% |

5.70% |

4.50% |

|

Source: Own study by Bankier.pl based on deposit rankings published from December 2022 to December 2025. |

||||

Staying with the leaders of the individual rankings, let's check how the maximum rates on deposits have changed for a month, a quarter, half a year and a year. The source of information are periodically published Bankier.pl rankings for the above-mentioned dates. The table above includes maximum rates for deposits available after meeting additional conditions, because these are usually offers with higher percentages.

Looking at the top offers over the next 12 months, it can be noticed that the best offers – apart from the above-mentioned NOWYdepozyt 1M HISY PROCENT deposit – have lower rates than in December last year. The biggest change in minus applies to offers for 12 months. Currently, you can get 4.50% on such a long-term deposit. on an annual basis. A year ago it was by 1.20 pp. more.

A significant reduction in profit also applies to half-year offers, which twelve months ago were the deposits that could bring the highest return on freezing funds, amounting to 7.60%. on an annual basis. The leader of the table was Nest Bank, which offered such interest rates on Nest Lokata Hello. The current rate is 1 percentage point. lower, but the leader remained the same. The given interest rate has been in force for a short time, on December 12 this year. Previously, for a significant part of the year, the bank offered 7.10 percent. on an annual basis.

The most popular 3-month offers among customers also saw discounts. The maximum rate decreased in 2025 from 7.50 to 7.00 percent. on an annual basis. Deposits for this term are also the ones that have lost the least in the last three years – from 8.30 to 7.00 percent. on an annual basis. This is a discount of over 15.60%. For comparison, the maximum rate on annual deposits dropped by over 45.10% in the same period.

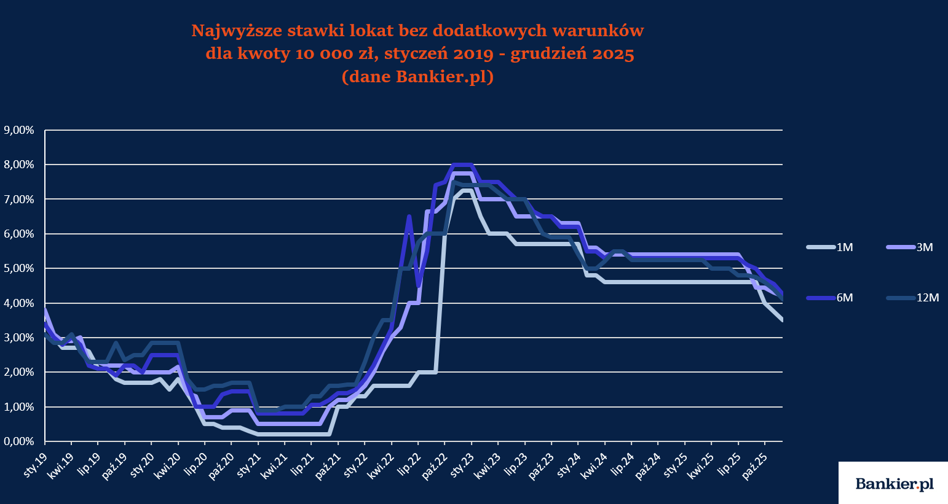

Equal discounts on deposits without conditions

Unlike offers with additional terms and conditions, deposits available as standard and without the need to open a personal account suffered to a similar extent. For all analyzed periods, the maximum rate can be reduced by between 1.05 and 1.20 percentage points.

The largest change in nominal terms concerns 3-month deposits. In their case, the cut was 1.20 percentage points. In December last year, the leader of the table was Toyota Bank, which offered 5.40 percent on Lokata Standard. on an annual basis. Currently, Inbank is at the top of the ranking, offering 4.20% on the Term Deposit. annually. Toyota Bank comes in second place, but with a much lower rate of 3.65%. on an annual basis.

On the other side of the comparison are half-year deposits, which have been cut the least among all the terms examined. However, the negative change is slightly smaller and amounts to 1.05 pp. Also in this case, there was a change of the bank at the top of the ranking and Toyota Bank lost the crown to Inbank. In the case of deposits for extreme periods, i.e. for a month and a year, the reductions in the last 12 months amounted to 1.10 percentage points, respectively. and 1.15 pp.

Taking into account the currently available rates on deposits without additional conditions, the leaders are offers for 6 months. By choosing the above-mentioned offer, you can count on 4.25 percent. on an annual basis. A slightly smaller percentage is included in the best offer for 3 months, i.e. 4.20%. on an annual basis. This is a change compared to December 2024. Back then, 3-month offers had the highest interest rates.

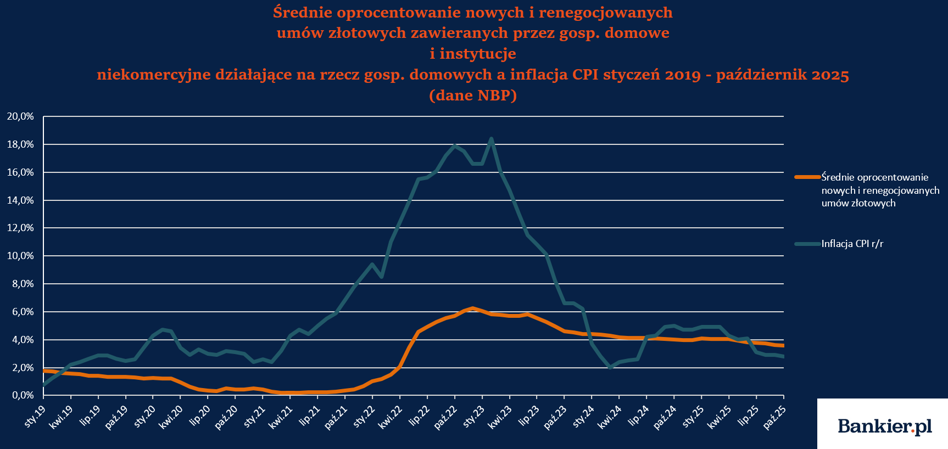

Inflation on target

The last 12 months have been marked not only by falling interest rates and rates on savings products, but also by decreasing inflation. We closed the year 2024 with a result of 4.70 percent, while the last available reading this year, i.e. for November, was 2.50 percent, which means that CPI inflation was then exactly within the target set by the National Bank of Poland. Therefore, last year's inflation projections from the National Bank of Poland, which assumed its increase to 5.60 percent, did not come true. The maximum level we encountered was 4.90%. and fell in the first quarter of 2025.

The level of inflation is also important, because it is with it that we should compare the interest rates on deposits to assess whether the client “made a profit” or rather lost money by freezing his funds on a given offer.

For this purpose, it is not enough to compare the deposit rate and the inflation rate for a given month. To assess the extent to which the client has minimized its negative impact on the value of money, it is necessary to compare its level with the deposit interest rate available before opening a given deposit. It will be easiest for us to compare the interest rate on a 12-month deposit opened in November 2024 with the CPI inflation on a year-to-year basis in the same month, but already in the following year. In addition, we cannot forget about capital gains tax (the so-called Belka tax), which actually reduces the interest transferred to the client's account.

CPI inflation y/y of 2.50%. entails the need to open a 12-month deposit with an interest rate of at least 3.10%. per annum in November 2024 to break even. The given interest rate is higher precisely because of the Belka tax. There was no shortage of such offers at the end of 2024. The maximum interest rate on a 12-month deposit with additional conditions was then 5.70%. per annum, and on a deposit without requirements 5.25 percent. on an annual basis. We also cannot forget about the higher rates that could be found on shorter-term deposits. Then, to compare them with CPI inflation on an annual basis, it would be necessary to calculate the interest rate for, for example, four consecutive quarterly deposits.

Next year's deposits will depend primarily on subsequent decisions of the Monetary Policy Council. According to the statements of MPC members, the space for cutting interest rates is getting smaller and no further changes should be expected earlier than March 2026.