After sharp price increases in 2021–2023, the housing market is entering a phase of clear stabilization. Prices per square meter remain high, but the growth dynamics has slowed down. At the same time, after a series of interest rate cuts, the availability of mortgage loans is improving. This revives demand, though buyers are still making decisions much more carefully than before the pandemic.

— The current real estate market is characterized by price stabilization, although in some of the cities we analyzed, there are visible trends on the secondary market that indicate a downward price correction, says Marcin Jańczuk, an expert in the Metrohouse real estate agency network.

— The market is completely filled with apartments for sale, which is why sellers must compete for a customer who, despite successive declines in interest rates, returns to the market quite slowly – adds the expert.

This means that buyers regained some of their negotiating power, and the average apartment sales time increased to approximately 3.5 months.

How do we compare renting and purchasing – real costs, not just the installment

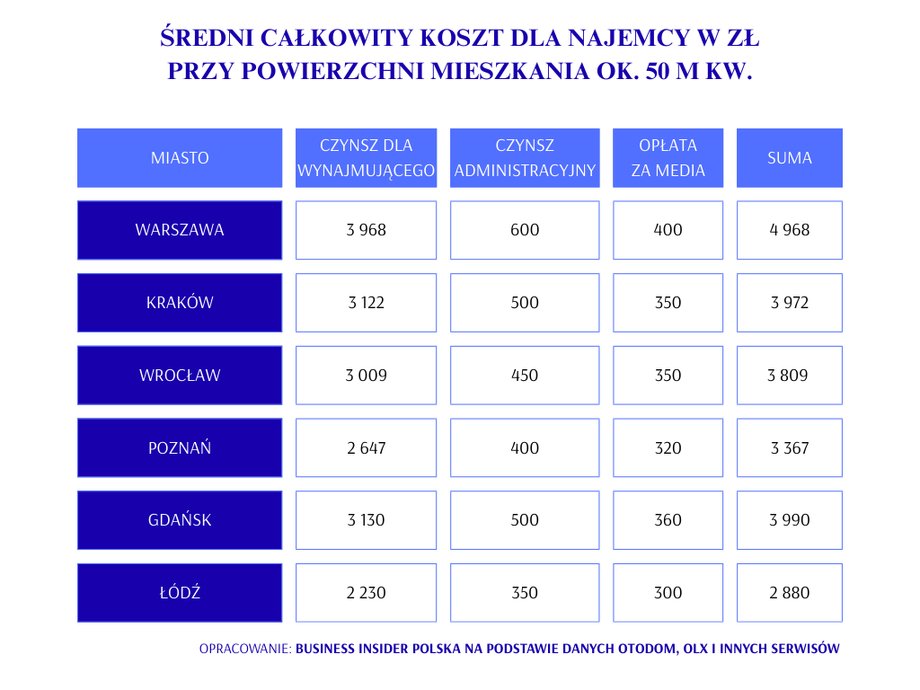

The analysis compared apartments with an area of approximately 50 square meters in six cities: Warsaw, Kraków, Wrocław, Poznań, Gdańsk and Łódź.

Average prices when purchasing an apartment on credit

|

Business Insider

Read also: We visited a ghost parking lot. It was built for almost PLN 70 million [TYLKO U NAS]

On the buy side included:

- loan installment (25 years, 80% of the value),

- administrative rent,

- utilities and ongoing maintenance.

Average rental prices

|

Business Insider

Worth reading: Strykers for Poland? We have a comment from the Ministry of National Defense

On the rental side:

- monthly rent,

- administrative rent,

- media.

Thanks to this, the full monthly housing costs are compared, and not only the loan installment itself compared with the advertised rent.

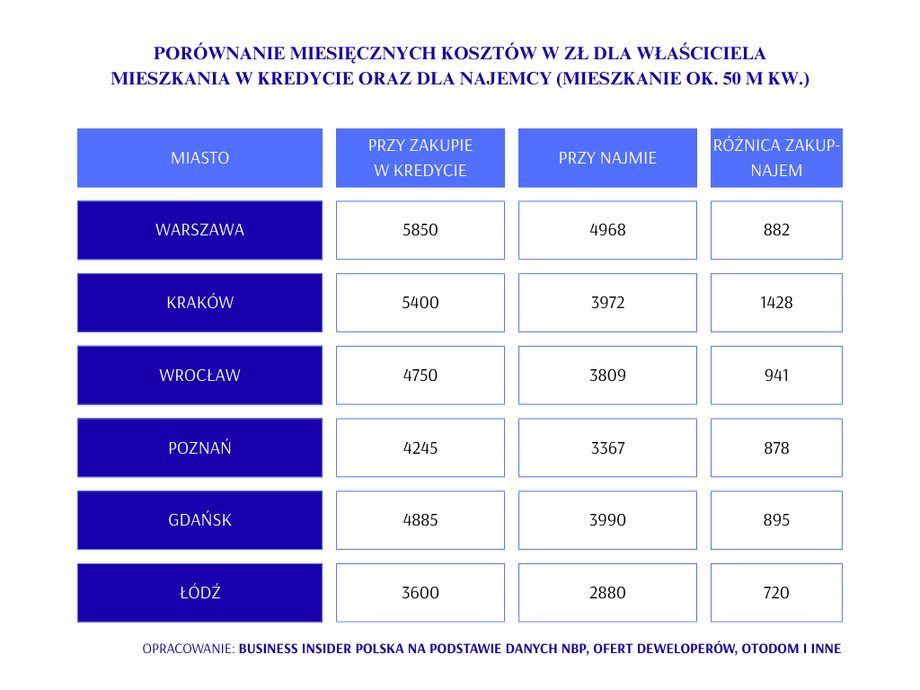

Hard numbers: in all cities it is more expensive to buy today

The comparison of the tables clearly shows that in all the analyzed cities the total monthly cost of owning a flat exceeds the cost of renting.

Monthly cost comparison

|

Business Insider

See also: Will the AI bubble burst sooner than we think? One factor is enough

This means that At current prices and typical lending conditions, renting is today a cheaper option in the short and medium term.

Example of Warsaw: difference of almost PLN 900 every month

For Warsaw, the total rental cost (rent, administration and utilities) is less than PLN 5,000. PLN per month, while the full cost of owning an apartment is on average approximately PLN 5,850 per month.

This difference doesn't even take into account:

- cost of own contribution,

- PCC on the secondary market,

- notary,

- intermediary commission,

- finishing of the premises.

In practice this means that For many households, renting today has a significantly lower monthly financial burden than purchasing.

Today, renting is a cheaper option in the short and medium term

|

photodaria / Shutterstock

Read: Sejm: Poland 2050 wants a revolution on the short-term rental market

Interest rates change the equation — but not immediately

The relationship between renting and ownership is changing with interest rate cuts. However, their impact on installments extends over time.

— Total drop in rates by 1.75 percentage points. it is a very large-scale movement. With an average loan of approx. PLN 450,000. PLN, this means annual savings of nearly PLN 8,000. zlotywhich is approximately PLN 650-660 less in the monthly installment – says Jacek Furga, president of the AMRON Center.

At the same time, he emphasizes that this effect will be visible gradually because interest rates usually update in three-month cycles. In the next several months, the relationship between rental and purchase costs may begin to equalize again.

The turn of 2022 and the trend slowly reversing

— For many years, loan servicing was more profitable than paying rent. This relationship reversed only in 2022, when interest rates have increased significantly — reminds Jacek Furga, AMRON Center.

— After the recent reductions, the situation will start to change again, although not overnight, he adds.

This means that the market is entering a transition period today: renting is dominated by short-term cost advantages, but purchasing may make sense in the long run.

Institutional leasing (PRS) – a growing alternative

The institutional rental segment is developing dynamically.

— In 2015, PRS's resources consisted of only a few hundred premises, while today their number exceeds 28,000. – says Patrick Pospiech, Director, Living Investments, JLL.

– Even though rent rates are rising, renting is still often more financially advantageous than paying off a mortgage installment for a similar apartment – adds the expert.

The JLL expert predicts that by the end of the decade, the PRS offer in Poland may exceed 50,000. apartments. Even though today it is about 2 percent. the entire rental market, this segment sets new standards: stable contracts, high quality and professional service.

Private vs. institutional lease – what tenants choose

– Leases from institutional owners are distinguished by the breadth of the offer, quality of service and guarantee of standard – says Maciej Piotrowicz, head of Urban Partners in Poland.

“Tenants can choose not only the location and size, but even the layout, equipment and color variant,” he assures.

For many people PRS becomes a compromise: higher standard than on the private market, but without the need for a loan.

Coliving – flexibility instead of ownership

A new form of living, increasingly visible in Otodom data, is co-living. This model of shared apartments or rooms with an “all inclusive” fee.

According to Otodom data, coliving attracts mainly:

- young specialists,

- people working on projects,

- foreigners,

- people relocating between cities.

Pros:

- no high entry costs,

- short contracts,

- fully furnished,

- utilities included in the price.

Cons:

- higher price per square meter,

- limited privacy,

- model mainly for singles.

Coliving does not compete directly with purchase, but effectively competes with classic short-term rental.

When does a purchase start to have an advantage?

A purchase may be financially rational when:

- the planned period of residence exceeds 8–10 years,

- own contribution is 30%. or more,

- interest rates will stabilize at a lower level,

- the apartment is to be an element of the construction of the estate.

In the shorter term, entry costs and higher monthly charges work against the purchase.

Conclusions for the market and households

- In all analyzed cities, renting is now cheaper than purchasing on a monthly basis.

- Institutional leasing systematically professionalizes the market.

- Coliving meets the needs of the most mobile tenants.

- The purchase remains a long-term and capital decision, not a cost one.

The housing market in Poland has entered a phase of new equilibrium. Loans are getting cheaper, but apartment prices remain high. Rental – both private and institutional – wins today in terms of monthly costs. Purchasing still makes sense, but mainly as a long-term stabilization and wealth-building strategy, rather than a way to quickly reduce the cost of living.

* To compile the data, the author selected several portals with rental offers (such as OtoDom or OLX), as well as offers from developers and agencies. The data collected in the tables are averaged based on sample offers for apartments with an area of 40-59 square meters. 20% was assumed for the loan. own contribution and loan period of 25 years at an interest rate typical for loans granted in the past year.