The Polish Financial Supervision Authority is analyzing the actions of Marcin Wojewódka. The expert shows how he violated the law

All transactions in PKP Cargo shares made by Marcin Wojewódka, vice-chairman of the supervisory board of PKP Cargo and previously acting president, are under the microscope of the Polish Financial Supervision Authority.

The sale and purchase of shares is nothing extraordinary, but the way of informing about them is important. In this matter, you must take into account the provisions of the EU MAR regulation (Market Abuse Regulation). And everything indicates that the information about the sale and purchase of shares by Marcin Wojewódka may have violated Art. MAR 19 We explain the details.

The rest of the article is below the video

Read also: PKP Cargo shares go up and down sharply. This rollercoaster is under the microscope of the Polish Financial Supervision Authority

Did Marcin Wojewódka violate the MAR regulation?

Attorney Magdalena Marczuk (formerly Szeplik) from the Gessel law firm explains that As a rule, MAR does not prohibit members of governing bodies from making transactions. They are prohibited in the so-called closed period, i.e. for a period of 30 calendar days before the publication of the interim financial report and in a few exceptional situations. This time they didn't happen.

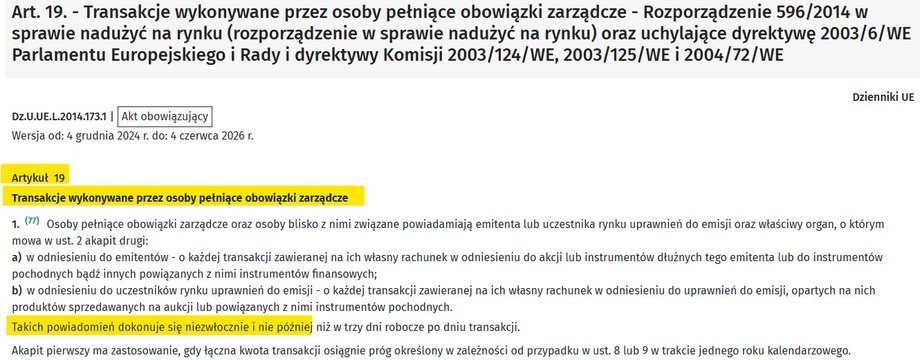

From January 1, 2020, persons discharging managerial responsibilities and persons closely associated with them should fulfill the obligation, however, the notification obligation in accordance with Art. 19 section MAR 1 Such notifications shall be made promptly.

According to Magdalena Marczuk notifications under Art. 19 MAR that were sent in connection with the transactions made were incorrect — both in terms of method and form. Why?

Article 19 of the MAR regulation

|

LEX

Why might there have been a violation of the MAR Regulation?

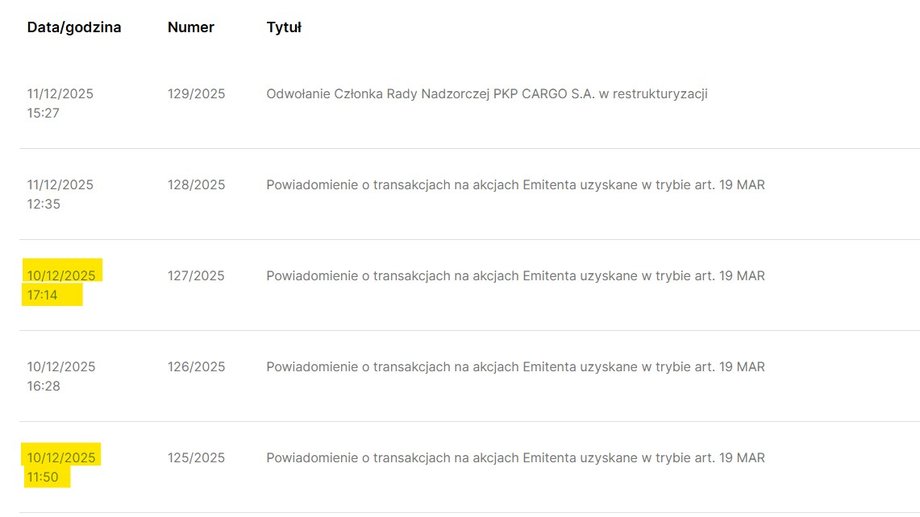

On the same day, December 10, two pieces of information were sent, first about the sale (current report no. 125/2025)and then about purchasing the entire pool of shares (current report no 127/2025). However, the latter information appeared only after the end of Wednesday's trading session, so investors could only react to it on Thursday.

Current reports of PKP Cargo. No. 125 and 127 concern the sale and purchase of shares by Marcin Wojewódka

|

PKP Cargo

Magdalena Marczuk believes that the MAR implementing regulations clearly indicate that the notification template should contain information on all transactions carried out on a given day by the obligated persons.

— To make public the full overview of the situationthe template should enable the presentation of individual transactions and their inclusion in aggregate form. Aggregate information should indicate the volume of all transactions of the same type in relation to the same financial instrument carried out on the same business day and in the same trading system or outside any trading system, as a single amount equal to the arithmetic sum of the volume of all transactions – explains Magdalena Marczuk. In her opinion, the legislator clearly emphasizes that the form should be collective and cover the entire day, which is important for the indicated “full overview of the situation”.

There is another issue that does not appear in the media discussion. It's about the way the data is presented in the notification, via your own attachment. — Creating your own attachment when all data should be included in the notification is an obvious violation – says Magdalena Marczuk. The case of sale and purchase of shares by Marcin Wojewódka shows how much “details” matter.

What do Marcin Wojewódka and the Polish Financial Supervision Authority say about this?

We asked Marcin Wojewódka whether he was aware that he could have violated the MAR regulation and whether he believed that he could have made a mistake by sending two messages instead of one about the sale and purchase of shares?

He replied that Due to applicable regulations, it does not provide any information or answers to questions regarding listed companies with which it is in any way associated, except in the form of stock exchange announcements.

We also asked the Polish Financial Supervision Authority:

1. Have the provisions of the MAR been violated by publishing two messages instead of one?

2. Will the Polish Financial Supervision Authority take action against Marcin Wojewódka?

3. What consequences may result from violating Art. MAR 19?

Jacek Barszczewski, spokesman for the Polish Financial Supervision Authority, replied that Wednesday's transactions in PKP Cargo shares are subject to analysis by the Polish Financial Supervision Authority from the point of view of the provisions of the MAR Regulation. – Let's share our findings when the analyzes are finalized – he assured, but did not declare when this would happen. In short, he did not answer anything beyond what he communicated on the X platform.

Selling shares in December and buying them on the same day? It may be about taxes

Selling and buying shares on the same day, especially in December, is a common practice among investors. Most often, they decide to make such a move when the stock exchange price of previously purchased shares falls. This is about taxes, and in practice, generating a loss that can be shown in the annual PIT settlement and deducted from the income from the sale of other shares or, for example, the sale of units in investment funds. The result of such operations is a reduction in tax on the sale of securities that generated profit for the investor in a given tax year.

Read also: PIT for 2024. We settle income and capital losses. There are novelties and pitfalls

Therefore, you can offset stock income against stock losses. For example, if if an investor sells shares at a loss, buys them on the same day, and next year their price increases, the investor will be able to deduct the loss generated in 2025 from the income earned in 2026.

Currently income from funds must be accounted for in the same way as income from the sale of sharesand thanks to this you can combine income and losses in one category, which means it is possible to offset losses from shares with profits from funds.

In practice you can compensate: :

- losses due to redemption of fund units with income from the sale of shares,

- losses from the sale of shares with income from the redemption of fund units,

- losses from the redemption of fund units with income from the redemption of other units of capital funds.

Moreover, plosses can be settled once (up to a maximum of PLN 5 million) or over five consecutive years if the income does not allow the loss to be deducted once. The rules set out in Art. apply to the deduction of losses. 9 section 3 of the Personal Income Tax Act.

This applies to both income and losses from Polish funds (e.g. investment funds and ETFs) and from foreign funds.

Let's add that you cannot deduct losses, e.g. from the sale of shares or funds with income such as dividends or interest (e.g. from bank deposits). They are still billed separately. You can learn more from the article entitled “PIT for 2024. We settle income and capital losses. There are novelties and pitfalls”.