There used to be an abyss between them, now it's just a narrow canyon. The interest rates on floating-rate and fixed-rate mortgages have become closer to each other. There is even a bank on the market where the variable variant is currently cheaper than the frozen rate.

A few months ago, based on bank simulations prepared for the Bankier.pl rankings, we pointed out that the space separating fixed and variable mortgage interest rates has shrunk. Two interest rate cuts later, we check what such a comparison looks like in the new circumstances. We expected changes and they are clearly visible.

Let us recall that the fate of the fixed versus variable rate relationship was a story in two acts. Until autumn 2021, loans with periodically fixed interest rates were initially more expensive than those based on the “WIBOR plus margin” model. A borrower who chose a fixed-interest mortgage (not very popular at that time) paid a certain premium for the certainty of the fixed installment. As it soon turned out, this strategy paid off with interest when interest rates started to rise.

From the first months of 2022, the situation is reverse. Loans with a periodically fixed rate tempt (of course, at the moment of incurring the obligation) with lower rates than their floating-rate counterparts. It can be said that we have to pay a premium for the chance to reduce the installment in the future. Whether such an “option” is worth betting, of course, is not known in advance. The choice between two variants of calculating the cost of borrowed funds is one of the dilemmas that plague borrowers. Now it seems even more difficult, especially if the potential debtor wants to focus only on the financial dimension of the problem.

October mortgages – the situation is getting interesting

In monthly reports, we show banks' offers for a typical household. In October, 10 banks presented their simulations in both fixed and floating rate versions. Let us remind you that only temporarily fixed interest rates are currently offered by two institutions – Bank Millennium and BNP Paribas Bank.

Maximum difference between a fixed rate for 5 years and a variable rate in the same bank was in the last ranking -0.67 pp. It was definitely lower than at the beginning of the holidays, when it reached 1.27 pp. It is also no longer obvious that the starting variable interest rate is higher than the fixed rate in the same institution. BOŚ is currently the only bank where we have recorded this inverse relationshipand the “spread” was 0.19 pp.

However, looking at the differences in offers within individual banks does not give a more complete picture. That's why we checked again what space separates them the lowest fixed rates from the lowest variable rates in the perspective of the entire market.

The distance is getting smaller

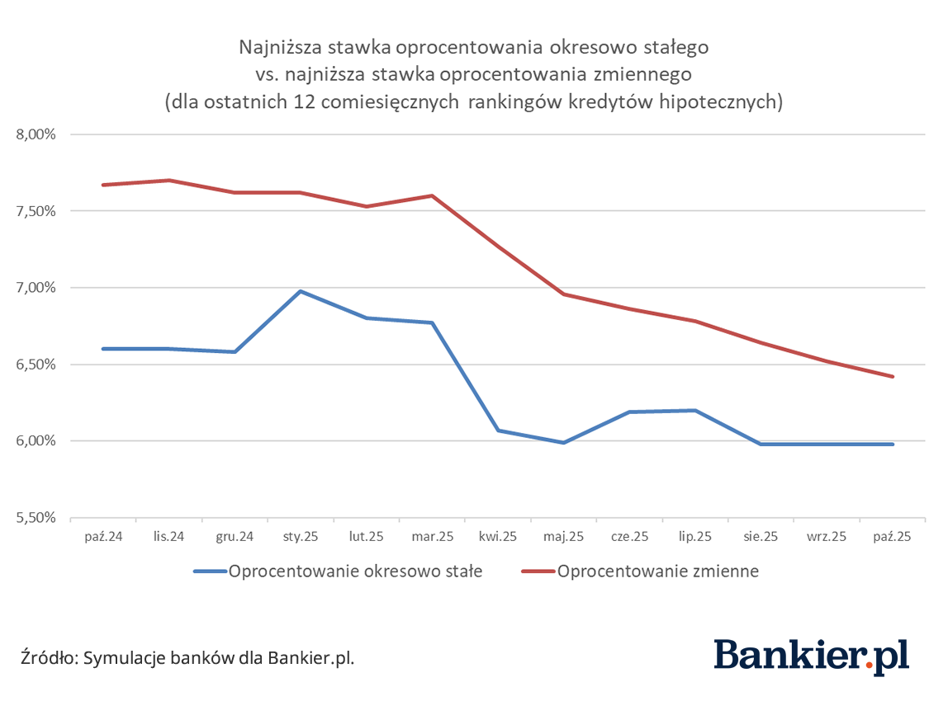

For each of the last 12 Bankier.pl mortgage loan rankings, we have selected the offer with the lowest interest rate in the fixed- and floating-rate mortgage categories. It is worth emphasizing that these were not always the winners of the rankings in which we take into account the total cost of the loan, which also includes additional elements (mandatory insurance, commission, etc.).

The chart confirms the current trend since 2022 – the “best” fixed interest rate is always lower than the variable starting interest rate. Changes occur in the distance that separates these two options. Let's go back exactly 12 months. In October last year, the best rate on the market for a periodically fixed interest rate was 6.6 percent, and for a variable one – 7.67 percent. The distance between these points was therefore over 1 percentage point.

In October 2025, the gap is the lowest for the last 15 rankings. The best “variable” and “fixed” proposals are separated by only 0.44 percentage points. In other words, a drop in the WIBOR rate by approximately 0.5 percentage points would be enough to make the cheapest loan with variable interest rate today as attractive as the loan with the lowest fixed interest rate (currently) on the market.

We also notice unification of rates in the case of variable interest. The distance between the highest and the lowest was only 0.38 percentage points. and was the lowest in the examined series since July 2024. Interestingly, this happened at a time when the differences between WIBOR 1M, 3M and 6M rates increased significantly (since spring 2025).

History doesn't have to repeat itself

As we approach the end of the interest rate reduction cycle, the rates of both mortgage loan options will likely continue to converge. However, the scenario known from earlier years, i.e. the exchange of “variable” and “fixed” prices, does not have to repeat itself. This time, not only market factors are at play.

Let us recall that the financial supervision in Poland strongly expressed its support for fixed-interest mortgages, and banks had to declare what part of their portfolio such products would ultimately constitute. Lenders, at least some of them, will probably want to maintain a certain balance in the sales structure and may use price incentives.