Now, officially, representatives of Smyk Holding, a leader in the industry of products for children in Poland, announced the intention to carry out the first public offer of shares, including the issue of new shares and the sale of some of the existing shares.

“The offer will be addressed to individual and institutional investors in Poland and selected international institutional investors, as well as to qualified institutional buyers in the United States of America. Smyk plans to apply for the admission and introduction of shares on trading on the regulated market of the Warsaw Stock Exchange” – we read in a message.

Smyk wants to enter the stock exchange. The president comments

“Our goal is to achieve the position of a leading retail seller in the omnichannel model in Central and Eastern Europe. We believe that this is a good time to invite new investors to the group of our shareholders and debut at the WSE in Warsaw”-pointed out Michał Grom, President of Smyka.

“We intend to allocate revenues from the issue of new shares to strengthen the company's financial profile and to finance further development” – he added.

The offer will include new shares broadcast by Smyk and the sale of parts of existing shares by AMC V Gandalf – currently the only shareholder. In turn, indirect shareholders are the Growth Capital AMC V fund, president Michał Grom and other minority investors. After IPO AMC V Gandalf, he will remain a majority shareholder, and Michał Grom plans to maintain (indirectly) a controlling package.

Earlier speculation regarding the amount planned to be obtained from IPO has not been confirmed. Smyk expects you Gross revenues from the issue of new shares will amount to about PLN 150 million and will be allocated to strengthen the company's financial position by partial repayment of bank debt and to finance further development strategy.

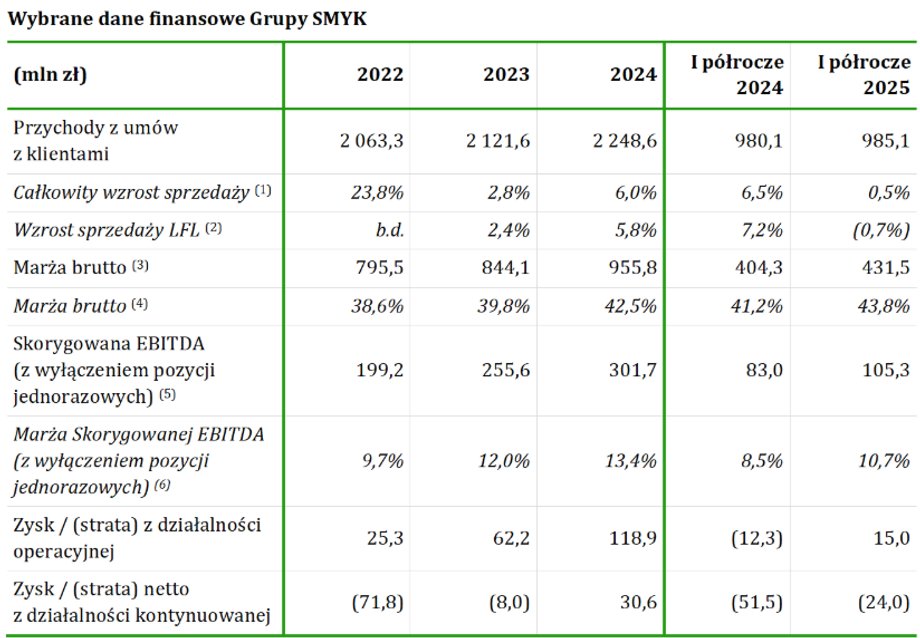

Smyk network and financial results

The main brands of Smyk (Cool Club, Smiki, Kayokki and Nowear) are strategic for its activities. In 2024 they were responsible for 51.5 percent. revenues from contracts with clients, which amounted to about PLN 2.25 billion.

At the end of June 2025, the sales network included 253 Own stores in Poland and 35 in Romania. The group also conducts operations in Ukraine (12 stores at the end of June 2025).

(1) The total increase in sales is calculated as a quotient of the difference between the total value of revenues from contracts with clients in the current period and the value of revenues from contracts with clients in the previous period and the total value of revenues with contracts with clients in the previous period. (2) LFL sales increase is calculated as revenues from contracts with clients in the current period reduced by revenues from customer contracts in the previous period divided by revenues with revenues shared by revenues with revenues shared by revenues with revenues shared by revenues with revenues. contracts with clients in the previous period for LFL stores. The store (stationary or online) becomes a LFL store after at least one full calendar year from the moment of opening (excluding closed stores, outlets and rebuilt stores). LFL sales are calculated as revenues from contracts with clients less wholesale sales, less revenues from contracts with clients in the Ukrainian segment, less revenue from contracts with clients in stores, which are not LFL stores, reduced by revenues from changing the reserve on the expected returns, reduced by the impact of the application of a permanent exchange rate for stores LFL. (3) The gross margin is revenues from contracts minus the value of goods and materials sold. (4) gross margin (%) is the ratio of gross margin to revenues from contracts with clients. (5) corrected EBITDA (excluding disposable items) is calculated as profit / (loss) network on the income tax, revenues and financial costs. depreciation and write -offs due to the loss of fixed assets, excluding the impact of disposable events, i.e. costs related to the change of the owner. (6) EBITDA corrected margin (excluding one -time position) (%) is calculated as the ratio of the corrected EBITD (excluding one -off position) to revenues from contracts with clients.

|

Kid