We have new data on digital customers in banks. This is not only statistics, but also a picture of everyday habits. We know in which banks customers log in most often, which can be a clue about whether online services are really comfortable there.

At the end of the second quarter of 2025, a total of 44.6 million bank clients had a total of e-banquet. Only 28.9 million customers were actively logged in. This means that about two out of three account owners really came to their bills, commissioned transfers and checked the history of online operation. The penetration of active users was 64.9 percent and although there is an increase compared to previous years, it still means that a third of customers with access to electronic banking is not logged at all.

29 million active digital banking clients

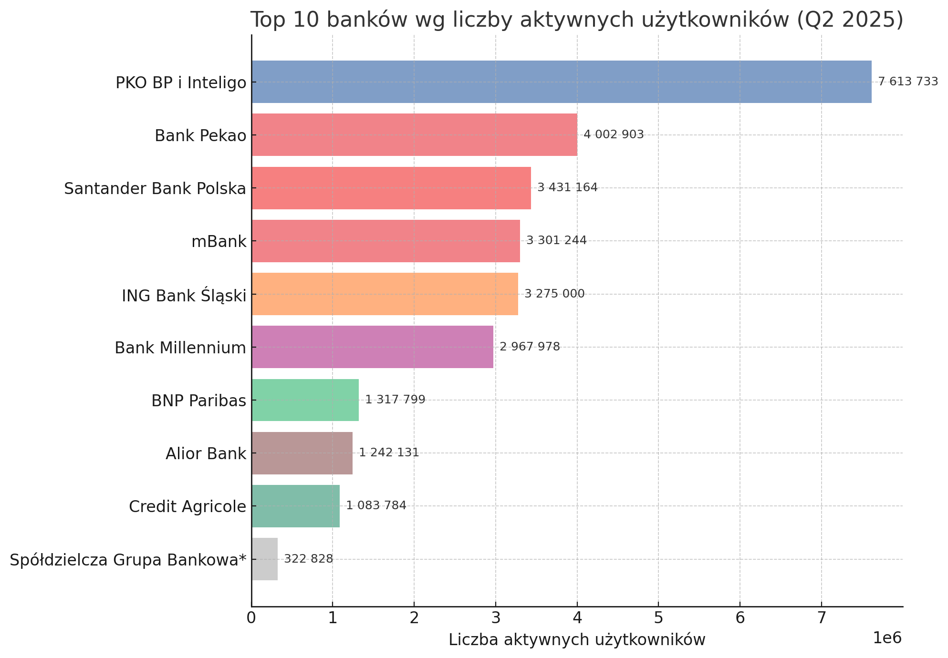

The biggest players dominate the market. PKO BP together with Inteligo boasts 7.6 million active customers and is a definite leader in absolute numbers. The second is Bank Pekao with a result of 4 million, and then Santander with 3.4 million and mBank and ING with about 3.3 million active each one. Five of the largest ones gathers three quarters of all active users in Poland, which shows that the market is strongly concentrated.

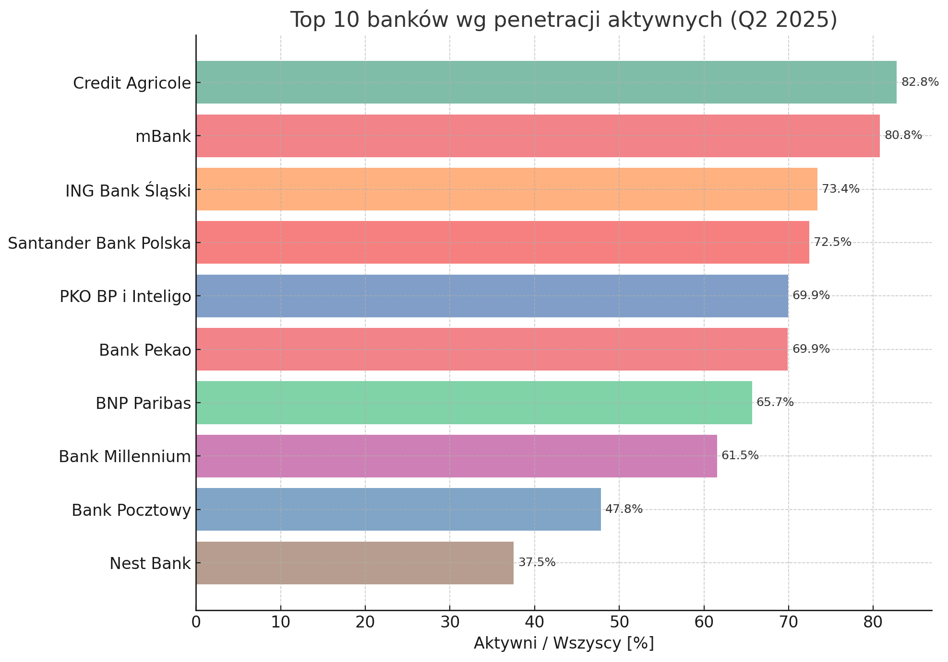

However, the number itself is not everything. The proportion is equally important, i.e. how many customers with access are actually logging in to electronic banking. And here the image changes. Activity indicators look best in Credit Agricolewhere over 82 percent of customers with access actually use online services. He also records very high activity mBank – over 80 percent and also ING Bank Śląski, Santander Bank Polska and PKO BPwhich have indicators above 70 percent.

Advertisement

At the other extreme there are banks that have large customer bases, but relatively few are logged in. This is Alior Bank – only 29.5 percent of customers with access are active. Nest Bank reaches less than 38 percent, and Bank Pocztowy less than 48 percent. This means that a large part of the clients of these institutions formally have a signed contract, but they do not use it in practice.

Why is this happening? On the one hand, this may indicate a more conservative customer profile, on the other – the comfort of digital systems. Where logging in and performing basic operations is fast, intuitive and friendly, customers log in regularly. Where the application is more complicated or requires additional steps, many users do not check their invoice online or the phone at all.

It is also worth looking at the dynamics of changes. In the second quarter of 2025, Credit Agricole noted the largest increase in the number of active in relation to the previous quarter and year, which shows that a small institution can effectively attract customers to digital channels. Stable increases can also be seen in Pekao, PKO BP and mBank, while Nest and Postal are struggling with declines, which signals the problem with maintaining customers with applications.

More and more mobile customers

A separate picture gives a look at mobile banking. More and more banks clients are logged only through the smartphone, giving up computers. In practice, this means that the application becomes the main channel of contact with the bank. The data show that in the second quarter of 2025 the number of active mobile users was the vast majority among all active. For mBank or ING, Mobile is the basic channel, and in PKO BP or Santander a group of customers is growing, who log in only by phone. This is a significant change, because the application in the phone is no longer only for checking the balance, but it has become the center of daily payments or transfers to the phone number.

The market is still growing, but it is clear that the rate of growth of new contracts is faster than the growth rate of actual activity. This means that banks have to focus not only on acquiring customers, but above all on their activation. For customers, however, it is a signal that it is worth paying attention not only to the price offer or promotions, but also to the quality of the mobile application. Because it is she who decides today about whether electronic banking is a daily tool or just a formal addition.