In the heart of the global armament industry: who are the biggest sellers of armament and what is the place of Romania in the trade of weapons

The armament industry has transformed into an indicator of global strength and influence, in the context marked by geopolitical tensions. According to Stockholm International Peace Research Institute (SIPRI) data, the “weapons industry” does not only mean the manufacture of weapons, but also a complex military services ecosystem – from Information Technology, Intelligence and Operational Support – which supplies the defense mechanisms of a state.

A group of economists from the National Bank of Romania, coordinated by Daniel Dăianu, analyzed the global evolution of this industry, from 2002 to the present, based on SIPRI data, and the results have been published in Euromonitor. What are the conclusions?

The reconfiguration of the market

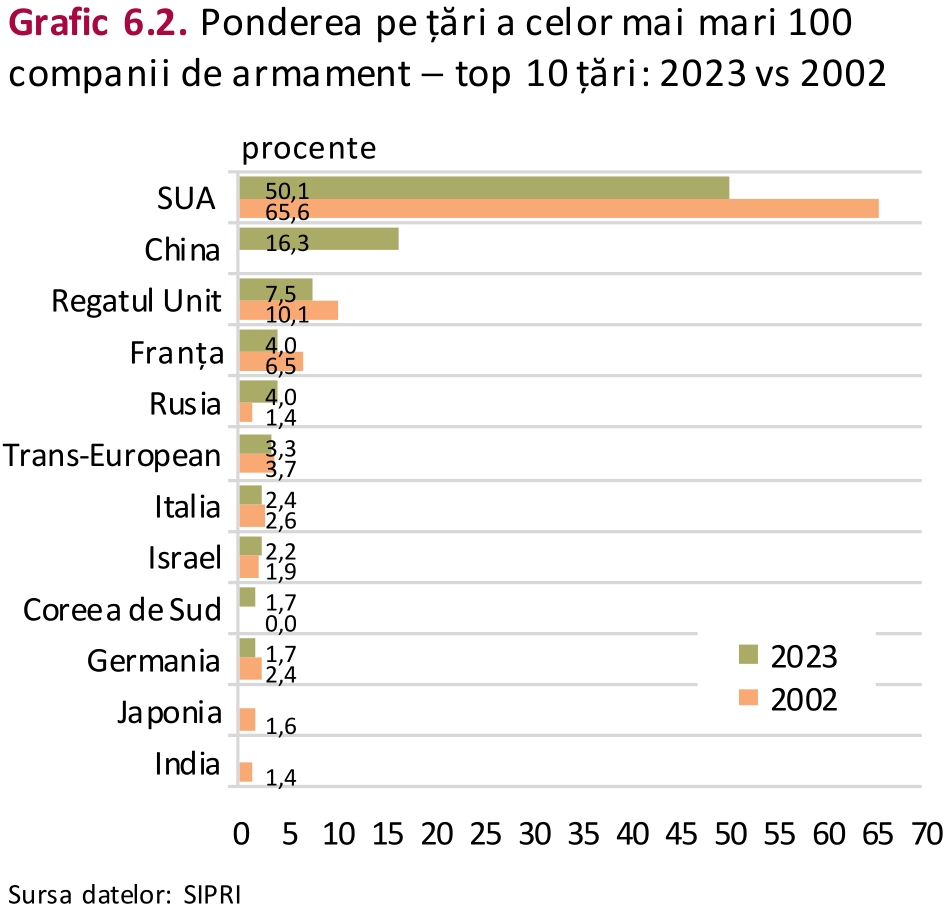

The US dominated the armament market, with a share that oscillated between almost 70% in the early 2000s and just over 50%, currently. However, the year 2015 marks a turning point: China penetrates steeply in the world top, bringing 7 companies directly in the first 25, after revenues. This ascension of Beijing meant not only the increase of the global turnover, but also a reconfiguration of the forces ratio: the US remains leaders, but they are no longer alone.

Against this background, the global armament market is kneaded and transformed, as strategic conflicts and interests change.

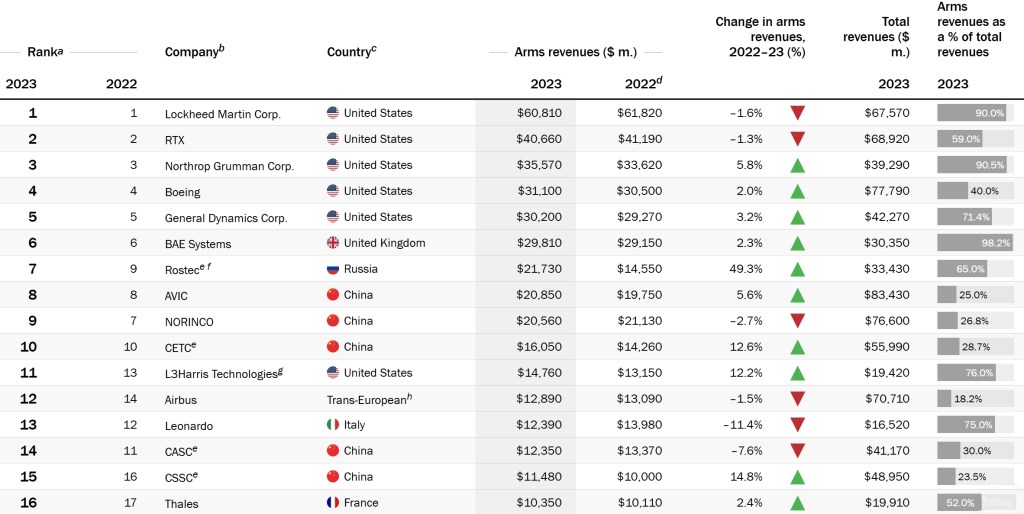

The 100 largest companies in the global armament industry made $ 632 billion revenues in 2023, representing an increase of 2.8% compared to the previous year, the quoted analysis shows.

The analysis of the SIPRI data regarding the total revenues from the sales of weapons of the first 100 companies producing armament and providing military services for the period 2002-2023 (expressed in constant prices 2023) indicates three distinct phases of development.

The first phase (2002-2010) illustrates a constant expansion, with income increasing from $ 331.2 billion to $ 528.1 billion, probably supported by Iraq and Afghanistan conflicts and modernization programs.

This ascending trend was reversed in 2011-2014, when the industry registered a contraction up to $ 452.1 billion, most likely reflecting the impact of the financial crisis and budgetary reductions in the field of defense.

The third phase (2015-2023) marks a return, with a sudden increase of 17.7% in 2015, followed by a stabilization at a level of approximately $ 630 billion, corresponding to the intensification of geopolitical stresses and accelerating the military modernization programs at a global level

Romania's place in the weapons industry

Romania, although it does not appear among the world giants -none of the 111 local companies enter the top of Sipri -, has its own story. The domestic defense industry is fragmented, with a more active private sector than the state.

In private there are three times more employees, and the sales of private companies are eight times higher than those of the state controlled companies. However, almost half of the state business is supported by Romarm, a company that, towards the end of the analyzed period, begins to lose ground.

However, Romania remains not only an isolated producer, but becomes a key player at European level as an weapon importer.

From the SIPRI data it turns out that Romania was an important beneficiary of weapons exports from two European countries, between 2020-2024. Romania represented 15%of the total armament exports of Norway, ranking as the third largest recipient of the Norwegian military equipment (28%) and Ukraine (21%). Also, Romania was the third largest weapons importer in Switzerland, absorbing 18%of Swiss exports, after Spain (24%) and Denmark (18%).

Trade with weapons – who, whom sells

In 2020-2024, transfers to Europe increased by 155%, and those to the American continent by 13%. All other regions registered decreases: Asia and Oceania, with 21%, the Middle East, with 20%, and Africa, with 44%. This reconfiguration probably reflects the impact of the Ukraine war on traditional armament flows and changes in regional security priorities.

The structure of global exporters presents a high concentration, the five major suppliers-USA, France, Russia, China and Germany-controlling 72% of the world market in 2020-2024, Euromonitor shows.

The United States has strengthened their dominant position, delivering armament to 107 countries-a market share more than four times higher than the next ranking.

France is the second world exporter, with 9.6%, increasing from 8.6% in the previous period. Russia has reduced its exports by 64%, its share on the global market decreasing to 7.8%, compared to 21%in 2015-2019.

The decrease started before 2022, in the context of reducing orders in China and India. Subsequently, the decline was emphasized as a result of the reorientation of the production to the internal needs and the sanctions imposed by the Western states. China had a relatively stable position, with 5.9% of global exports, while Germany registered 5.6%.

Two-thirds of US transfers to Ukraine were used in stocks to ensure fast delivery

Regarding the types of armament exported, the information available from SIPRI data shows that the US has dominated the provision of long -range terrestrial attack (45% of global exports to 7 states), having additional deliveries to 13 states for this type of armament.

Almost two thirds (71%) of US transfers to Ukraine were used in stock armament to ensure fast delivery. France has delivered fighter jets to Greece and Croatia, as well as artillery, missiles and ships to Ukraine, after the Russian invasion of February 2022. For other major exporting countries, the SIPRI document (Sipri, 2025) does not provide specific details about the types of military systems exported during 2020-2024.

The five major weapons importers-Ukraine (8.8%), India (8.3%), Qatar (6.8%), Saudi Arabia (6.8%) and Pakistan (4.6%)-absorbed 35%of global imports between 2020-2024 (SIPRI, 2025).

Ukraine-invaded by Russia from February 2022-registered the most important growth, of 9,627%, compared to 2015-2019, due to the Western military support. India registered a decrease of 9.3% of imports between the two periods, and in terms of suppliers, the share of imports from Russia decreased from 55% in 2015-2019, to 36% in 2020-2024, while the acquisitions in France increased to 33%.

Ukraine received armament mainly from the US, Germany and Poland

Qatar registered a 127% increase in imports, while Saudi Arabia reduced imports by 41%, after the completion of major procurement programs. Pakistan increased imports by 61%, maintaining China as the main supplier, with 81% of imports (SIPRI, 2025).

Ukraine received armament mainly from the US (45%), Germany (12%) and Poland (11%), most transfers being in the form of military aid. The types of systems received included anti-aircraft defense systems, artillery, armored vehicles and long-range rockets, the SIPRI material showing that 71% of American transfers have been used armament so as to ensure quick delivery.

In 2024, the remote attack capacity of Ukraine was improved by 300 km ray missiles, with the source of France, the United Kingdom and the US, as well as fighter jets from Denmark, the Netherlands and Norway.

SIPRI analysis on the evolution of military spending in 2024 shows that they registered the highest annual increase after 1988, reaching a level of $ 2,718 billion, the data published in Euromonitor shows.