Borrowers overpay mortgages faster than last year, according to the credit information office. Admittedly, it is far from records that were made in 2022, but the trend may soon strengthen the decrease in interest rates on liabilities.

Compared to the times of the interest rates soaring, the latest mortgage data on overpayments may seem to be of little impressive. We would like to remind you that the slogan “We get rid of the loan” turned out to be a hit of the first half of 2022. The debtors scared the dramatically growing installments, and many of the borrowers with savings remembered the option of overpaying the commitment.

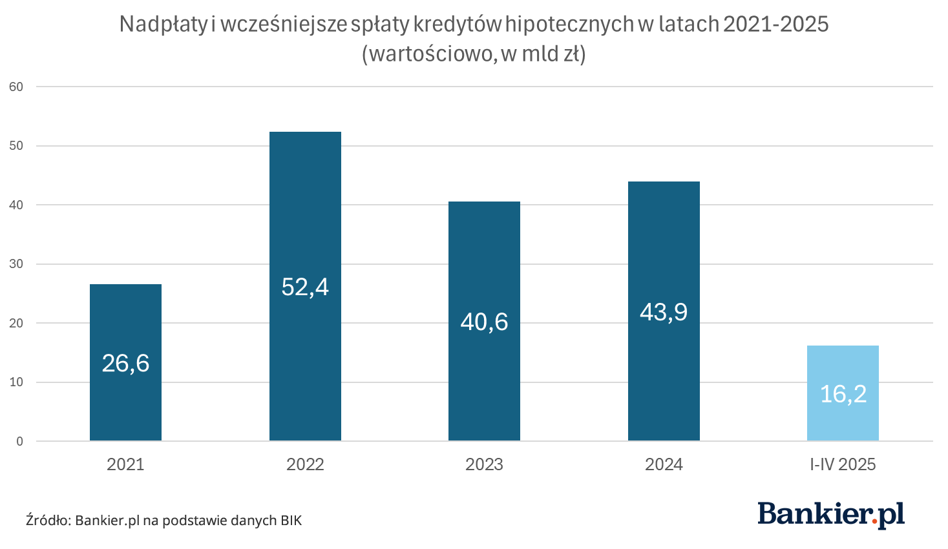

The effect was immediately visible in statistics. In 2022, the sum of overpayments and earlier total repayment of mortgage loans was twice as high as in 2021. A total of PLN 52 billion flowed to the banks. Interestingly, the peak of this “mobilization” fell for months before the introduction of credit holidays. Therefore, the trend could not be explained only by the influence of the statutory moratorium.

The latest data provided Bankier.pl by the Credit Information Bureau shows that the pace of overpayment remains stable, with a slightly growing trend. Throughout 2024, flows They were much lower than in the record 2022, but still second in size in the history of our market. In the first four months of 2025 a total of PLN 16.2 billion flowed into the banks. If it were assumed that the pace would remain stable, last year's result would be pierced.

The decrease in installments is conducive to “biting” the debt

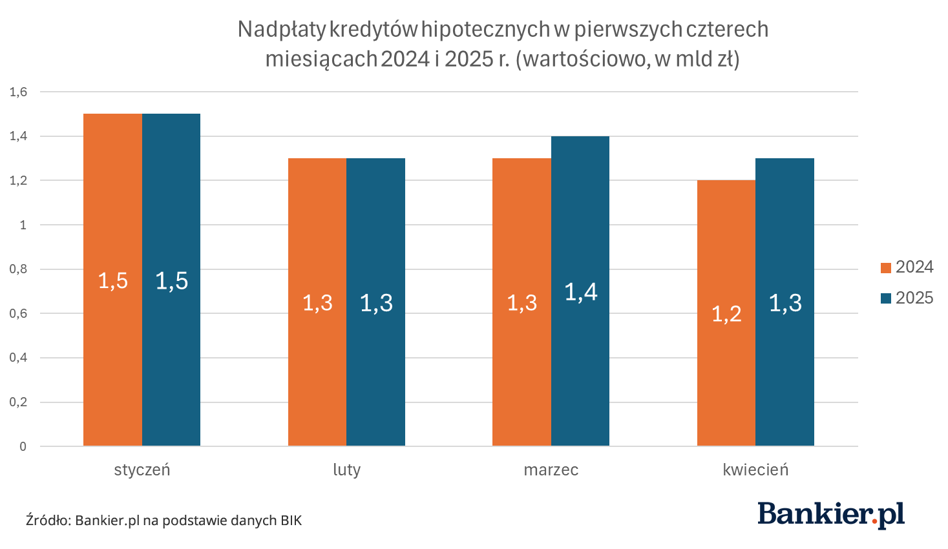

If we reach for comparing the latest data with the results from the same period last year, then you can see signs of a growing trend. In the case of partial payments (overpayments) of mortgage loans, the first two months fell identically to January and February 2024. In March and April, “adding” to the installments slightly accelerated.

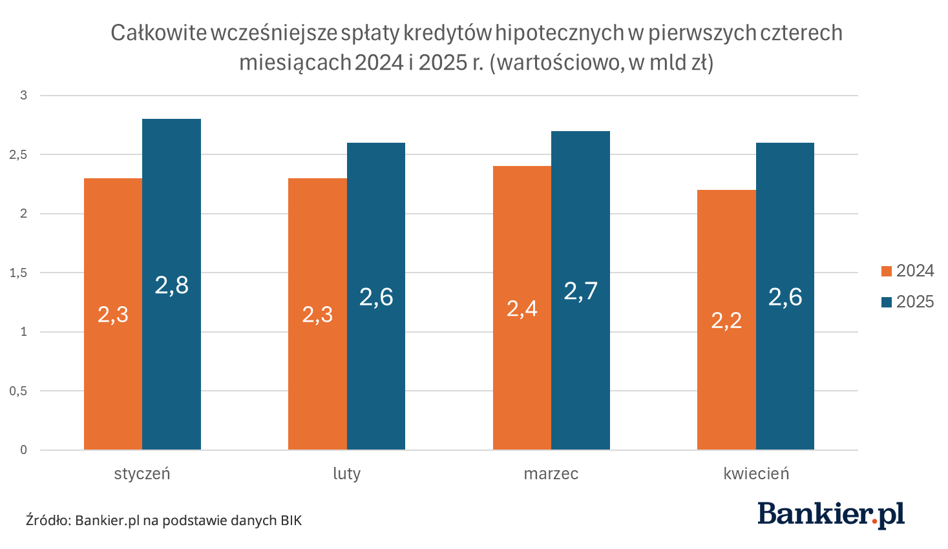

Definitely a different picture brings a comparison of total earlier repayments, i.e. a situation where the borrower gets rid of his liabilities (what, attention, may also be the effect of refinancing). In each of the first 4 months of the year, the amounts were PLN 0.3-0.5 billion higher than in 2024.

The decrease in interest rates, which began with a May decision of the MPC, can strengthen both the rate of hypothek overpayments and earlier repayments. The borrower, having at their disposal the funds released in the budget thanks to falling installments (in floating percentage loans, still dominating in the bank's portfolio), have the option of using them to get rid of debt faster. This solution can be attractive, e.g. compared to safe forms of saving available today on the market.

It is worth noting that BIK data take into account primarily larger one -off overpayments – lowering the balance by at least 10 percent. debt. Therefore, minor regular overpayments escape the meters constructed in this way. However, if the borrowers accumulate reserves and then overpay the obligation once, then some such transactions (especially for older accounts) would be included in the office.

Earlier total repayments resulting from debt refinancing are thrown into one bag with other possible scenarios in BIK databases. The category “total earlier repayment” includes in the data presented by BIK all cases in which the account is closed at least 6 months before the date resulting from the schedule.

Mortgage loans are still decreasing

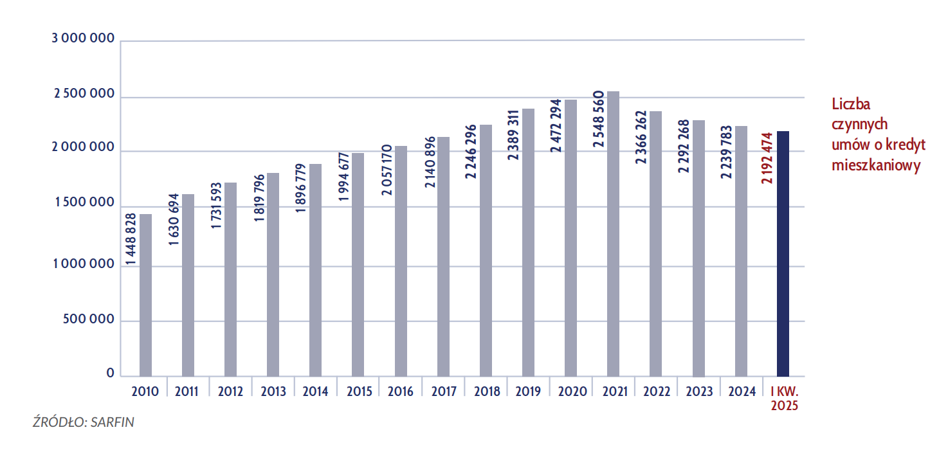

Although the last data on the sale of mortgage loans look good, it is worth recalling that there is a “deletion” of households. The borrowers are still paying off their liabilities faster than they make them. This trend has not been reversed if we look at annual data since the mortgage time in 2021.

WW KW. 2025, there were 2.19 million active contracts. During the quarter, this number decreased by 2.1 percent, In comparison with the first quarter of 2024, it fell by as much as 4.29 percent. In 2021, when a historic record was broken, 2.54 million contracts were active.