ECB reduces interest rates to 2%, but Lagarde says future discounts are less likely. What does that mean for your rates

Photo source © AlbertopHotography | Dreamstime.com

Interest reduction is a quarter percentage point and comes after inflation in the euro area has dropped under the target in May

The long-awaited Thursday's decision is the eighth discount with a quarter percentage of the central bank in a year. From June 2024, the authorities establishing the interest rates have halved the loan costs from a 4%peak.

There were few reactions to this decision on the markets, remaining unchanged from the dollar, at $ 1.142, writes Times.

Most analysts provide that the unexpected growth of the euro from the tariff ads made by the US President in April, on the occasion of “Liberation Day”, combined with lower energy prices and a potential increase in imports from China, will maintain the increases of consumption prices in the euro area under control.

“The risk that inflation will not reach the goal has increased clearly,” wrote Carsten Brzeski, the head of the Global Macroeconomic Division of ING, in a note published after the decision.

The central bank reduced the inflation prospects for this year to a medium term target of 2%, compared to 2.3% forecast in March.

He also warned that “the uncertainty around commercial policies” will “affect investments and business exports, especially in the short term.”

Christine Lagarde suggests that future interest rates discounts are now less likely

Christine Lagarde said that “I have concluded almost a monetary policy cycle that managed a series of shocks”, a remark that could be understood as an implicit indication that future interest rates are less likely.

She added that this reduction in the interest rate has placed the ECB “in a good position” to cope with the uncertainties that “profile in our path”.

What does this mean for Romanians with loans in euros

For Romanians with rates for loans in euros with variable interest, this will translate into a slight decrease in these rates.

The impact of reducing interest rates will be felt differently by banks' customers, depending on the type of contract (we refer to credit agreements in euros with variable interest, those with fixed interest being not affected).

As a rule, banks update their interest on loans at 3 or 6 months depending on the contract each one has. At the next update the new level of interest will be incorporated, and the rates could decrease marginally.

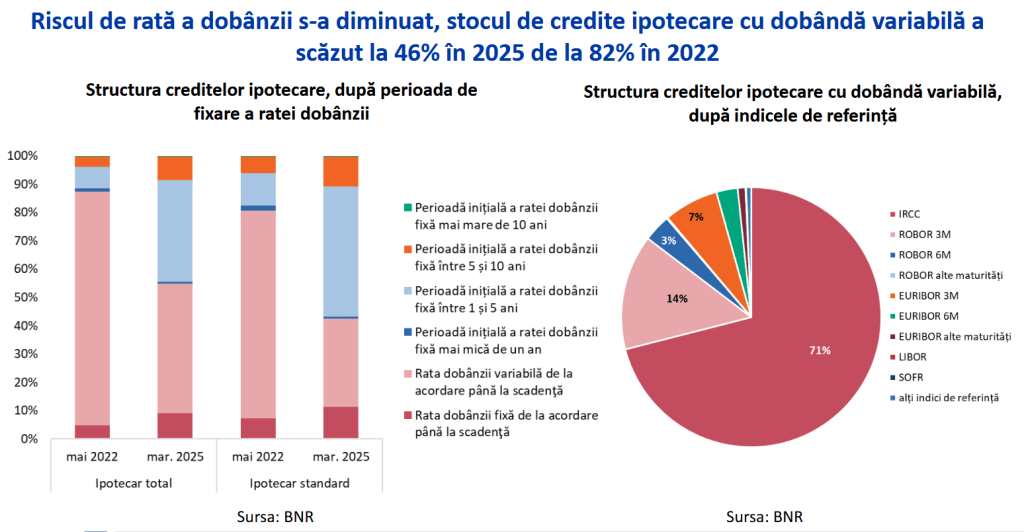

The Romanian banks have small exposures on the mortgage loans with the interest anchored to Euribor, the exposure being higher in the case of the credits granted to the builders and developers.

In the case of the latter, an important proportion of the credits of the Cre- the Acronimul Commercial Real Estate (94% percent, September 2024) is exposed to the risk rate risk, being granted with variable interest from granting to maturity. Of these, 34 percent have Euribor reference index at 3 months and another 30 percent ROBOR at 3 months. Only 4 percent of the volume of CRE credits is granted with fixed interest from granting to maturity.

In the case of the population, the exposure is much smaller.