The creditworthiness and stable prices of apartments that have been clearly growing since the beginning of the year meant that buyers supporting the loan can afford a larger apartment than a year ago. Even by nearly 11 sq m. – results from Bankier.pl data.

We have recently written about falling and at least stable in an annual basis of housing prices in various contexts. This time we decided to check how the rates dictated by sellers with at the same time growing creditworthiness, affect the area of the apartment available to buyers using a housing loan.

As it results from monthly analyzes carried out by Michał Kisiel, Bankier.pl analyst, we can talk about the growing creditworthiness in banks for five months in a row. In May, however, the increase already deserves to be called. The average of lenders' simulation increased by over 51 thousand. zloty.

I am talking about a simulation prepared since January 2024 for the family “two plus one” living in Warsaw. We assume that borrowers have a total of 15,000 at their disposal. zloty. A 29-year-old woman is employed on the basis of an employment contract for an indefinite period and earns 8,000. PLN net. Her 32-year-old partner has a similar situation, but slightly lower earnings-7,000 PLN per month.

In May, the creditworthiness calculated by thirteen banks – at the range of 957,000 – PLN 227,794. On average, it amounted to PLN 1,067 114 in the case of permanent interest rates and PLN 1,012,306 if the loan was based on a variable interest rate.

Apartment on a loan greater by up to 11 sq m.

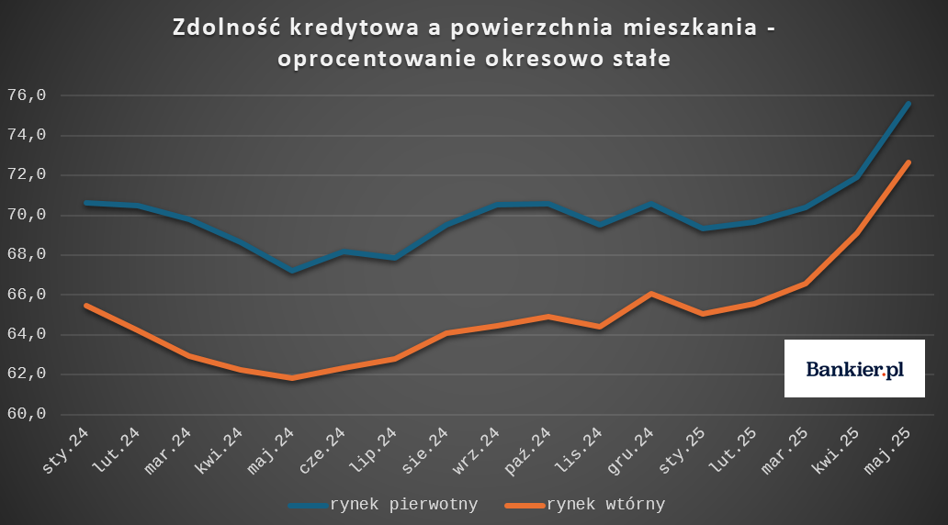

If this data is combined with average offer prices observed in April 2025, it turns out that a model family wanting to buy a flat from the primary market, assuming a 20 % own contribution and a periodically permanent interest rate, could afford an average of 75.6 sq m.

When deciding on a second -hand premises, the maximum available area would be 72.7 sq m.

This is the highest result in the history of measurements and about 3.7 sq m. more than a month ago and from 8.4 to 10.8 sq m. more than in May 2024, when the purchasing capabilities were the lowest.

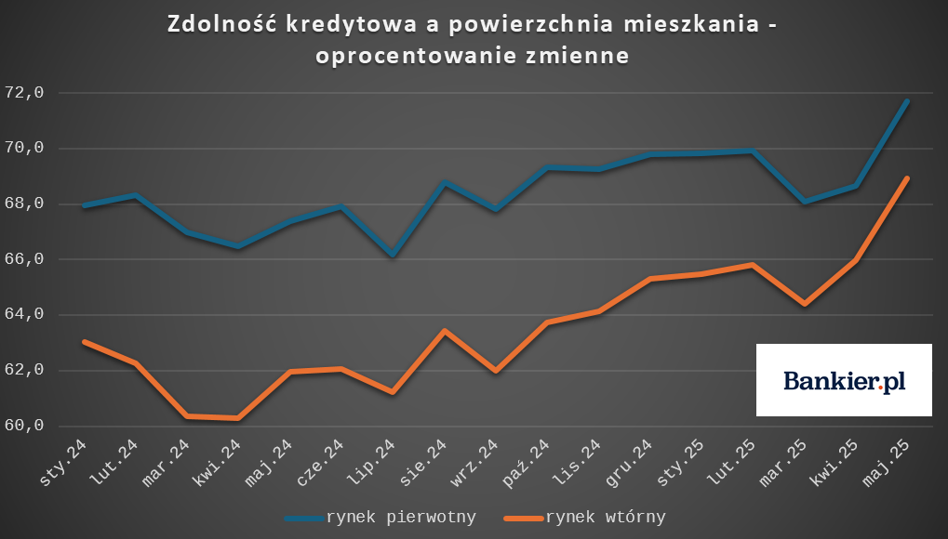

For slightly smaller apartments, taking into account the above assumptions, they could be allowed by the buyers using a mortgage with a variable interest rate. It would be: 71.7 sq m respectively. in the case of the primary market (+3 sq m Mi +4.3 sq m) and 68.9 sq m. In the case of the secondary market (+3 sq m Mi +7 sq m).

Ability to M5

What will the same situation look like, if we consider the average offer prices listed in the case of individual meters? In the case of the most expensive per square meter, but at the same time the cheapest in terms of total amount, pieces up to 40 sq m. The matter is simple. Both the creditworthiness calculated by the most cautious bank and the loan amount offered by the most “generous” would allow full freedom as to the surface.

The situation is different in the case of larger apartments with an area of 40 to 59 sq m. and the lowest recorded creditworthiness. In the first four months of 2025, it allowed the purchase of a flat from the secondary market with an area of 49.9 sq m at the average offer price. In February to 55.8 sq m. in April. Only the May leap of creditworthiness meant that the loan from the most cautious bank could afford to buy an apartment with a maximum area in a given range.

The latest creditworthiness data, in turn, give hope looking for larger apartments, especially on the secondary market. The ability proposed by the winner of the May statement would allow the purchase of an apartment from a secondary market with an area of 84 sq m. – at 4 sq m. larger than a month earlier and by 10.2 sq m. greater than in May 2024.

Taking a loan from a bank characterized by the lowest installment ratio for monthly income, i.e. in fact proposing the lowest creditworthiness, they could take possession of an apartment with an area of less than 66 sq m. In the previous months, buying an apartment in this area at an average offer price would be impossible.

Developers go to “downsizing”

Although in recent months buyers using a loan can be easier to change in offers and decide on larger meters, developers' actions are different. According to the data of the Central Statistical Office, the entire last year was marked by the decline in the average area of apartments put into use.

Considering all, over 103 thousand apartments in multi -family buildings, which developers transferred for use, their average area was 51.4 sq m. – by 0.4 sq m. less than a year ago. For comparison, in 2017, new apartments measured on average nearly 59 sq m. in 2008 record 67.8 sq m.

Mkz