The Pacific Yap Islands were, at the beginning of the 20th century, one of the most inaccessible places on Earth. A subtropical paradise, nestled in a tiny archipelago more than 300 miles from Palau, the nearest neighbor.

Almost no one had ever visited him, until 1730, when a group of bold Catholic missionaries set a small base on the island. After a year, when the supply ship returned, he discovered that the islands were not a fertile ground to evangelize them, writes Felix Martin in his book “Money”. In fact, all the members of the mission had been massacred in the first months of residence. Yap was left to his will for another forty years.

Much later the first commercial post of the German company Godeffroy and Sons was set up, after Spain sold the Germans for $ 3.3 million (in today's money).

The integration of the Yap archipelago into the German Empire had a great benefit: it brought to the world one of the most interesting and unusual monetary systems in history

This is after the visit of a brilliant and eccentric American adventurer, William Henry Furness III. Descendant of a prominent family in New England, Furness had been trained as a doctor before being converted to anthropology and to do a good renowned with his journey into Borneo.

In 1903, he paid a two -month visit to YAP and published a large study a few years later. It was immediately impressed that, although the main island takes you “only one day of walking” it runs long and wide, Yap has a remarkably complex society. There is a caste system, with a tribe of slaves and “neighborhoods” in which the fishermen or warriors lived. There was a rich tradition of dances and songs, which the Furness recorded for posterity.

But, without a doubt, the most striking thing that Furness discovered on Yap was their monetary system.

The Yap economy could hardly be called developed. Their market included only three products – fish, coconut nuts and the only luxury at Yap, sea cucumber.

There was no other changeable merchandise to talk about; they had no agriculture; There were few arts and trades; The only domestic animals were pigs and, since the Germans had arrived, a few cats.

In view of these conditions, Furness expected exchanges between goods to be done by barter. But no!

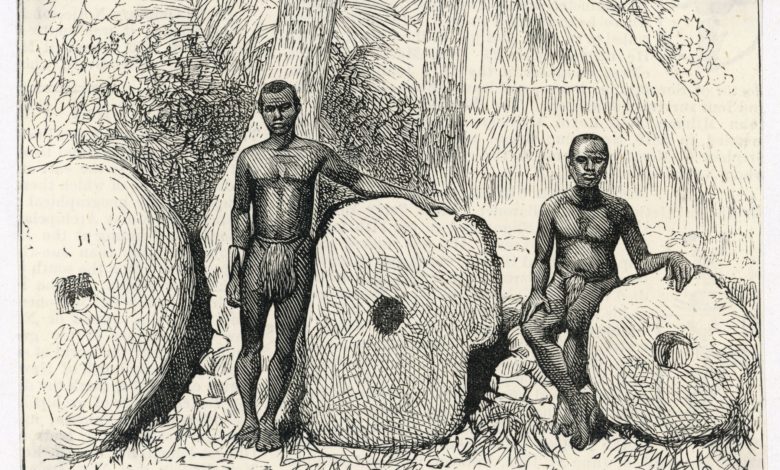

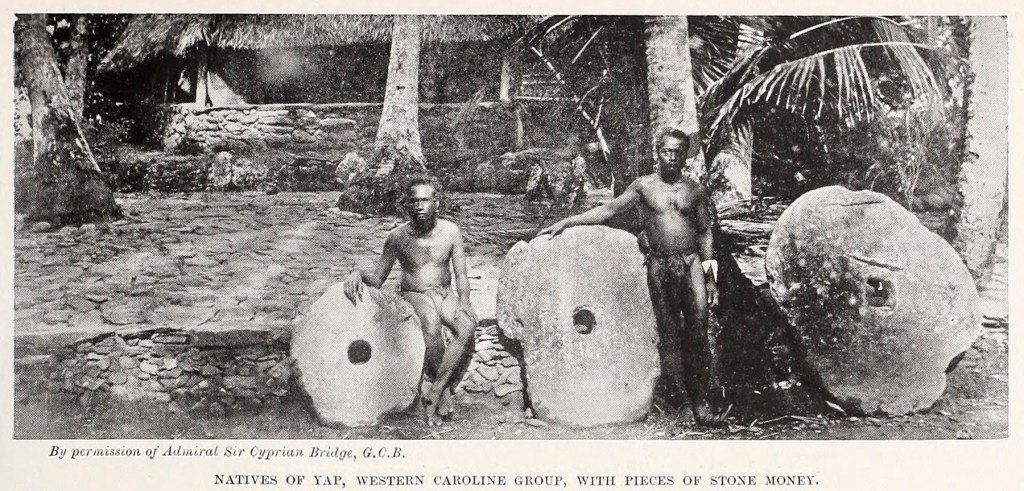

Yap had a highly developed money system. It was impossible for ant to notice this when he set foot on the island, because their coins were extremely unusual.

Consist of “fai” – “large, solid, thick stone wheels, with a diameter between 0.3 meters and 3.6 meters, having in the center a hole that varies in size depending on the diameter of the stone, through which a pillar can be introduced to withstand the weight and facilitate the transport”, writes furness in the book “Stone Island”.

These “stone money” were initially extracted on Babelthuap, an island about 300 miles away, in Palau, and were mostly brought to Yap.

The value of the coins depended mainly on their size, but also on the fineness of the granulation and the intensity of the limestone.

At first, Furness believed that this bizarre form of currency would have been chosen precisely for her extraordinary weight in handling: “When it takes four strong people to steal the price of a pig, breaking can only be a very discouraging occupation,” he writes. In fact, the thefts of faces are almost unknown.

As time passed, he noticed that the physical transport of the FEI from one house to another was very rare. There were numerous transactions – but the contracted debts were compensated for each other, with any outstanding balance, waiting for a future exchange.

“The remarkable feature of this stone currency,” he wrote, “it is not necessary for the owner to hold it on his own. After the conclusion of a fair, his new owner is quite pleased to accept the simple recognition of the property, even if the currency remained within the former owner.”

When Furness expressed his astonishment to this aspect of the Yap monetary system, his guide told him an even more surprising story:

[Therehewasinthevillagenearafamilywhosefortunewasundeniable-recognizedbyeveryone-andyetnoonenoteventhefamilyhadeverputhiseyesorhandonthisfortune;sheconsistedofahugefairyButinthelasttwoorthreegenerationshewassittingatthebottomofthesea!ThecurrencyhadbeenshipwreckedduringastormwhilehewasintransitfromBabelthuapmanyyearsagoButthemereaccidentofhislossshouldnotaffecthiscommercialvalueThepurchasingpowerofthatstoneremainsthereforeasvalidasitwasvisiblysupportedonthefacadeoftheowner'shouse[Acoloeraînsatuldelângăofamilieacăreiavereeradenecontestat–recunoscutădetoatălumea–șitotușinimeninicimăcarfamiliaînsășinupusesevreodatăochiisaumânapeaceastăavere;aconstatdintr-unfeienormDarînultimeledouă-treigenerațiistăteapefundulmării!MonedanaufragiaseîntimpuluneifurtuniîntimpceeraîntranzitdinBabelthuapcumulțianiînurmăDarsimplulaccidentalpierderiisalenuartrebuisă-iafectezevaloareacomercialăPutereadecumpărareaaceleipietrerămâneașadarlafeldevalabilăcașicumarfisprijinităvizibilpefațadacaseiproprietaruluiWhen he was published in 1910, it seemed unlikely that Furness's eccentric travel journal would ever reach the attention of economists.

But finally, a copy came to a young Cambridge economist, recently detached from the British Treasury: a certain John Maynard Keynes.

The man who in the next twenty years would revolutionize the understanding of the world about money and finance was amazed. The book of Furness, he wrote, “brought us into contact with a people whose ideas about currency are more philosophical than any other country. Modern practice has a lot to learn from Yap Island practices.

John Maynard Keynes was right. The description made by William Henry Furness of the Stone Currency may seem at first to be just a picturesque base of money history.

But she asks some uncomfortable questions of money theory. Take, for example, the idea of many that the money appeared from the barter. When Aristotle, Locke and Smith made this statement, they only did it on the basis of deductive logic. None of them has ever seen an economy that works entirely through the exchange.

But it seemed plausible that such an arrangement had existed sometime. In this context, Yap's monetary system came as a surprise. This was such a rudimentary economy that it should have worked through the barter. However, it didn't work that way. On the contrary, it had a fully developed system of money and currency.

But if such a rudimentary economy already had money, then where and when there was a boss -based economy?

This question continued to disturb the researchers over the century after his ant about Yap has been published. As the historical and ethnographic evidence has accumulated, Yap has come to show less and less an anomaly.

As much as he was looking for, no single researcher was able to find a society, historical or contemporary, who regularly carry out trade in a barter.

Until the 1980s, the important anthropologists of the money considered that “the trocul, in the strict sense of market exchange without money, was never an important or dominant way of trading in any past or present economic system that we have concrete information,” wrote the American scientist George Dalton in 1982. Cambridge Caroline Humphrey in his book “Barter and Economic Disintegration”. Also, American economic historian Charles Kindleberger wrote in the second edition of the Financial History of Western Europe, published in 1993 that “economic historians occasionally argued that the evolution of economic relations has gone from a barter economy to a monetary economy and then to a credit economy.

As anthropologist David Graeber explained in 2011: “there is no evidence that it has ever happened, but we have a huge amount of evidence that has not happened.”[Nuexistăniciodovadăcăs-aîntâmplatvreodatădaravemocantitateenormădedovezicaresugereazăcănus-aîntâmplat”

However, Yap's story is not just a challenge for the explanation of conventional theory about the origins of money. It also raises serious doubts about the idea of what the money is. Conventional theory claims that money is a “commodity” to serve as a means of exchange – and that the essence of monetary exchange is the exchange of goods and services.

But Yap's stone money does not match this definition. It is hard to believe that someone could have chosen “large, solid, thick stone, diameter between 0.3 meters and 3.6 meters”, as a means of exchange – because, in most cases, it would be much harder to move than traded things.

In addition, there was no doubt: the residents of the Yap were curiously indifferent to the fate of the stones. The essence of their monetary system were not the stone coins used as a means of exchange, but something else.

If the stones were not a means of exchange, then what were they?

The answer is super simple. The money in Yap was not the Fei itself, but the credit accounts system and the compensation with which they kept. The faces were the “chips” with which these accounts were held. Coins and currency, in other words, are useful chips to record the basic credit account system and to implement the basic compensation process.

They may be needed in a greater economy than that in Yap, where coins could sit on the bottom of the sea and no one would think about questioning their owner's wealth.

The currency is not in itself is not money. Money is the credit account system and their compensation. Like modern banknotes, which are also some kind of chips. Most of the coins of our contemporary economies do not enjoy the physical existence, but consist of the balances of our account in banks. The only tangible device used in most monetary payments today is a plastic card and a keyboard. So it is not exaggerated to say that a pair of microchips and a Wi-Fi connection are a means of exchange of goods.

With a strange coincidence, John Maynard Keynes is not the only giant of the 20th century economy that greeted the inhabitants of Yap for the clear understanding of the nature of money.

In 1991, Milton Friedman, seventy -nine – extremely different from Keynes – also gave over the book of Furness. And he praised the fact that Yap escaped the conventional, but unhealthy obsession with the currency and acknowledged so transparently that money is not a commodity, but a credit and compensation system.

To win the praise of one of the greatest monetary economists of the 20th century can be regarded as an incident; To win the praises of both deserves all the attention.