The session on the WSE did not end as well as the quotations of the main indices suggested two hours before its end. Enthusiasm faded due to the pullback on Wall Street, but WIG managed to stay above the mark mainly thanks to the demand for shares of KGHM and Orlen, which together generated over half a billion zlotys in turnover. Orlen's share price climbed to the highest level since the beginning of 2019, and its valuation exceeded PLN 130 billion. The Polish giant is currently valued higher than, for example, Maersk – one of the global leaders in maritime shipping.

The WIG20 index gained 0.56%, reaching 3,412.74 points, although the index increased by over 1% during the day. The weaker end of the session, which demobilized demand, was a consequence of the pullback in the US. Wall Street initially welcomed the overdue report on the US labor market, but it seems that after analyzing the details, including the revision of the annual data, the enthusiasm has faded.

The European core markets followed the herd leaders and at the end of trading in Warsaw, the DAX was losing 0.5% and the CAC40 was falling by almost 0.2%. The indexes in Madrid and Milan were negative, but London looked positive, with the FTSE100 gaining about 0.9%.

Against this background, WIG20 still looked good, as did the broad market in Warsaw, represented by WIG, which gained 0.47%. This time, medium and small companies fared slightly worse, as mWIG40 gained 0.22% and sWIG80 increased by 0.08%. All indices are trading near their peaks. The turnover on the broad market was estimated at PLN 2.3 billion, of which PLN 1.8 billion concerned WIG20 companies, and almost PLN 570 million was traded on shares of KGHM (PLN 388.4 million) and Orlen (PLN 179.3 million).

From an expert's perspective: the important behavior of the dollar

According to Sobiesław Kozłowski, uncertainty may persist on the market until the end of the week. “This Friday there will be a reading of consumer inflation in the United States. Yesterday, retail sales were clearly weaker than expected, the question is whether it is a one-time surprise. One of the concerns is whether the issue of increased inflation in the context of rising metal prices is something temporary or something more permanent. That is why this inflation reading seems to me to be the key reading of the week,” he said.

“The data are clearly better than expected, which seems to reduce the confidence in two interest rate cuts by the Fed this year. The question is whether subsequent data will confirm this and whether the market will interpret it as an argument for the strengthening of the dollar. So far, the narrative has been that the dollar may be weaker for a long time. Meanwhile, the latest GDP reading in the United States was also higher than expected, so perhaps the dollar is too weak,” he commented on Wednesday's data from the US labor market.

“Now it is worth looking at the behavior of the dollar and the yields of American bonds. There is a clear reaction to EUR/USD, the question is whether Friday's inflation data will actually confirm today's payrolls reading. If so, it would be an argument for considering whether the dollar should strengthen, which would put pressure on emerging markets and raw materials,” he added.

KGHM revives after recommendations, Orlen with a new record valuation

KGHM was the leader in the WIG20 index on Wednesday, growing by 5.06%. The company effectively took advantage of the rebound in copper and especially silver prices on global markets. The price rebounded after Tuesday's sell-off, which was explained by the reaction to several negative recommendations.

Sobiesław Kozłowski notes that the copper concern is becoming more and more closely correlated with silver prices, and some investors may already be positioning themselves for the first quarter results, which the company will show on March 25.

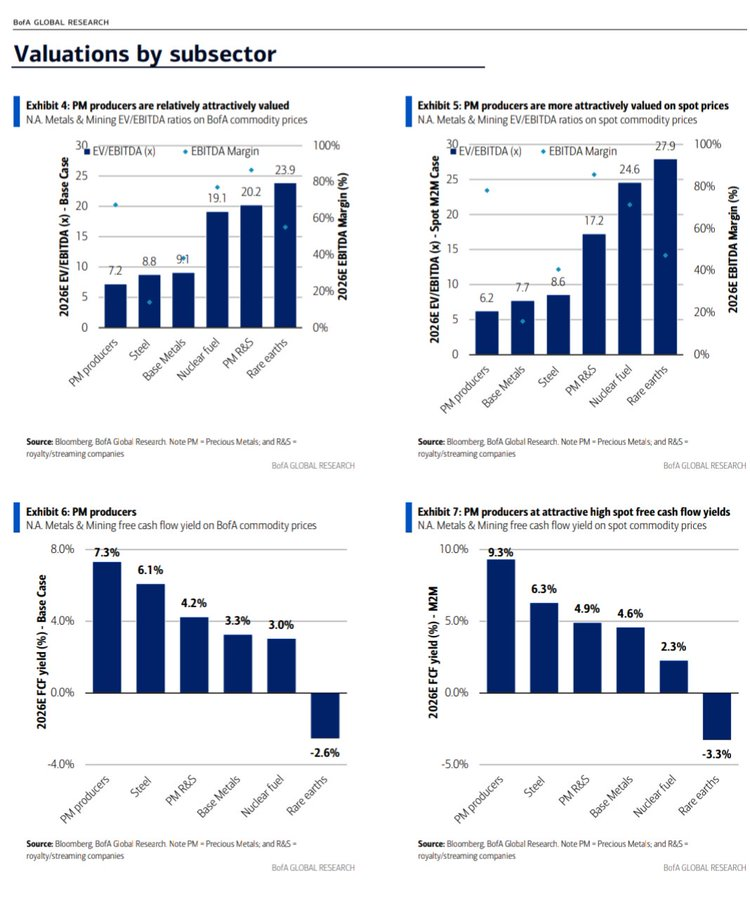

It is worth noting that in the popular Bank of America bulletin, precious metals miners are the cheapest commodity sector in terms of index valuation. They are characterized by, among others: the lowest total value of the company (Enterprise Value) to the EBITDA result, and on the other hand, they have the highest ratio of the company's cash generation efficiency in relation to its market capitalization, or in other words, the highest rate of return on cash flows.

Orlen's shares were also in the price, increasing by 2.51%. to PLN 111.90 and are the highest since the beginning of 2019, however, due to share issues related to the mergers with Lotos and PGNiG, the company's valuation is the highest in history and amounts to almost PLN 130 billion. During the session, the rate reached as high as PLN 112.18 and valued Orlen at over PLN 130 billion. Currently, with a USD valuation of USD 36.56 billion, the Płock company is worth more than such global brands as, for example, the Danish Maersk (USD 34.9 billion), one of the two largest shipping operators in the world, or the German Adidas (USD 33.2 billion).

The energy sector continues its streak, banks continue to withdraw

Orlen's strong share price, where energy is a strong business line, may be the result of a good period for this industry. The WIG-Energy index gained 0.98%, driven by PGE (3.37%) and Enea (1.68%). This sector remains one of the strongest industries on the Warsaw Stock Exchange in recent days.

In WIG20, the bottom of the scoreboard was again occupied by banks. The largest share of this blue-chip sector was lost by mBank (-1.87%), but declines also affected PKO (-0.67%), Alior (–0.76%) and Pekao (-0.48%). Only Santander (0.51%) was listed in positive territory among the largest banks.

The results of BNP Paribas BP caused a real sensation. The bank's price shot up by 7.38%. after the publication of the report for the fourth quarter of 2025, the net profit turned out to be 15.5%. higher than the consensus, and the dividend announcement is at the level of 50%. profit further fueled demand. Against this background, the rest of the sector, despite record NBP data on the profits of the entire Polish banking sector for 2025 (PLN 48.7 billion, an increase of 21.5% y/y), looked miserable, and the entire WIG-Banki lost 0.32%.

Referendum in JSW

In the mid-cap segment by 2.22%. JSW prices increased. Investors are looking forward to Thursday's referendum among the staff with hope. Employees' consent to suspending some benefits is a necessary condition for obtaining external financing and avoiding the scenario of drastic statutory restructuring.

Rotations at MSCI Poland

Changes in the prestigious MSCI Poland index brought a lot of emotions. CCC dropped out of the ranking (1.37%), and was replaced by Asseco Poland (-2.03%). However, the market reaction was far from textbook – Asseco's share price was falling, and CCC, despite the degradation, found its way to growth.