From the perspective of the entire housing sector, 2025 appears to be a moment of significant slowdown after the hot period of 2023–2024.

In the opinion of the vice-chairman of the Real Estate Committee at the Polish Chamber of Commerce it was neither a crisis nor a surprise – rather a natural consequence of the extinction of demand that had previously been artificially stimulated Safe 2% loan program

When this impulse disappeared, the market entered a normalization phase, characterized by lower transaction volume, greater caution among buyers and a clearly increasing selectivity of investors.

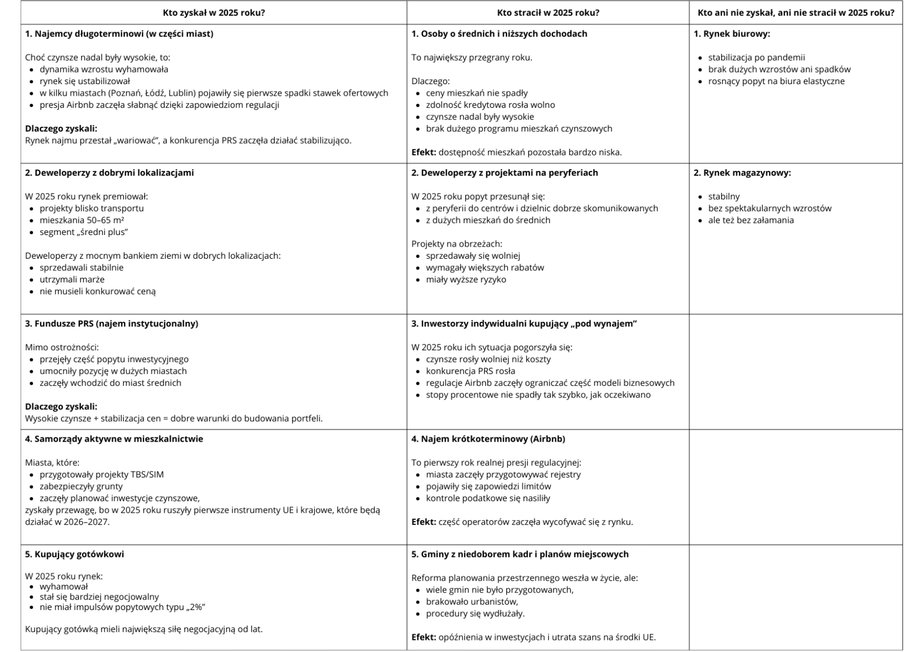

Krystyna Helińska believes that 2025 brought a phenomenon on the rental market that she calls “expensive stabilization”

|

KIG

Read also: Changes in taxes from January 2026. Check whether you will not lose

According to Krystyna Helińska the result was price stagnation and, in some segments, even correction. In the largest agglomerations, the dynamics of apartment price growth dropped to 2-5%. y/y, which can be considered a safe pace, close to the foundations of household income.

Importantly, the market began to “punish” overvalued products. Micro-studio apartments, low-standard apartments or investments carried out on the outskirts of cities have lost their attractiveness, and in some locations real declines in offer prices have been recorded.

Against this background, the program stands out positively Credit 0 percent Contrary to fears it did not lead to another demand shock. Its limited scale, more precise criteria and timing made it more stabilizing than destabilizing. According to the expert, this allowed us to avoid a repeat of 2023, when the market lost contact with the real availability of apartments. The year 2025 proved that State intervention may cool emotions instead of fueling them — as long as it is designed carefully, argues the vice-chairwoman of the Real Estate Committee of the National Chamber of Commerce.

Rental market and PRS: price stabilization and the first real regulations

The year 2025 brought a phenomenon on the rental market that Helińska calls “expensive stabilization”. Rents remained at high levels, but the dynamics of their growth significantly weakened. In regional cities such as Łódź, Poznań and Lublin, we observed a flattening of the price trend. This is a clear contrast to the years 2022–2024, when the market reacted nervously to every migration or inflation impulse.

Demand pressure remained mainly in Warsaw and Krakówi.e. in the largest business and academic hubs. Even there, however, the increases were much weaker than a year earlier. The rental market has become more predictablewhich should be considered a positive change from the point of view of tenants and investors – even if the price level still remains a barrier for many households.

In the institutional rental segment (PRS), the upward trend was maintained, but the pace of expansion decreased significantly. Expensive capital and limited access to financing forced the funds to revise their strategies. The priority became operational efficiency and the finalization of commenced investments, rather than aggressive portfolio expansion. At the same time, we saw an interesting geographical turn – institutional investors increasingly became interested in medium-sized citiesoffering higher rates of return and less competition.

The year 2025 was also a symbolic but very important event the beginning of the end of the “free American” in short-term rental. Kraków, Gdańsk and Warsaw have started work on registers and limits, which should be treated as the first real step towards civilizing this segment. In the expert's opinion regulation of short-term rentals is one of the key elements cooling the real estate market in 2025 and a condition for restoring the residential function in city centers.

Developers, regulations and demography: caution instead of expansion

For the development sector, 2025 was the year of risk management. New supply was significantly limited, which resulted from both high construction costs and uncertain demand. Decisions to launch new projects have been verified many times, and the industry has increasingly chosen the “less but better” strategy.

However, the most serious problem remains supply side. The lack of investment land and the lengthy administrative procedures effectively choked off new investments. Despite planning reforms initiated in 2023, 2025 showed how uneven the capacity of local administration is. Staff deficits in municipalities mean that even with a better legal framework, the pace of decision-making remains unsatisfactory, which invariably frustrates investors.

Summary of the Polish real estate market in 2025

|

National Chamber of Commerce

See also: Apartment prices in 2026 will change. First expert forecasts

Strategically, developers increasingly directed capital towards the luxury segment, mixed-use projects and cooperation with the PRS sector. At the same time, 2025 confirmed the growing importance of sustainable construction. Contractor prices stopped rising, and the fight against inflation was replaced by the fight for energy efficiency. Prefabrication, renewable energy and ESG standards have become a market minimum, not a competitive advantage.

Finally, Krystyna Helińska draws attention to: the impact of social and demographic trends. Young Poles are increasingly choosing to rent – not out of choice, but out of necessity resulting from high apartment prices and limited creditworthiness. On the other hand, the aging of the population generates a growing demand for smaller, accessible and barrier-free apartments, as well as for senior projects. These changes are already forcing us to change our thinking about the supply structure.

The balance of 2025 is, in the expert's opinion, bittersweet. The price and cost chaos has been brought under control, and the market has entered a phase of greater predictability. At the same time, fundamental problems – the supply gap, lack of land and bureaucracy – remained unresolved. The year 2025 was a time of great braking and caution, which, however, did not bring a structural breakthrough. This is the baggage with which the industry enters 2026.