Investors rubbed their eyes with amazement when they saw Dino Polska's valuation shrink by 17% in response to the company's poor results. The drastic decline in the EBITDA margin to a record low of 6.9% is just one of the dark clouds over the network. Inside the company, there is an open dispute between employees and the management over labor costs, and the lack of dividend and the announcement of further price fighting only fuel market panic. The shares of the Polish trading giant, which are the favorites of foreign capital, are becoming a hot potato and their prices are falling.

Dino Polska's financial results for the fourth quarter of 2025 caused a wave of disappointment on the Warsaw trading floor. The Dino Polska share price dropped by over 17% on the WSE on Friday, March 27. up to PLN 33.10. This was the lowest price for shares of the Polish supermarket chain since October 2024.

In May last year, the price reached a historic peak, climbing to PLN 56.20 and valuing the company at PLN 55 billion.

Currently, the price has dropped by 41% from the peak, and the valuation has dropped below PLN 33 billion. The attention was drawn by Fathersturnover, which after two hours of trading exceeded PLN 390 million and accounted for almost half of the turnover of the entire WSE, which at 11 a.m. amounted to PLN 830 million.

The company, which for years was considered a model of profitability and efficiency in the retail sector, faced a new market reality. Although revenues continue to grow at a double-digit rate, the rapid erosion of margins has alarmed investors, undermining analysts' optimism.

Dino's historic result

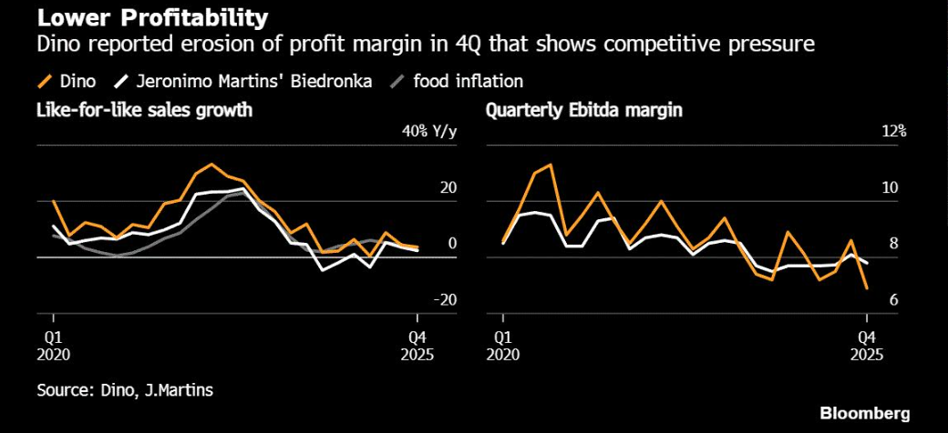

This turned out to be the most painful point of the report EBITDA margin, which decreased to 6.9% in the fourth quarter of 2025. For comparison, a year earlier it was 8.1%. This is a record low result in the company's stock exchange history, which directly translated into a decline in EBITDA by 2.8% year-on-year, to PLN 613.5 million.

Analysts are almost unanimous in their negative assessment of these data. Quoted by Bloomberg Michał Potyra from UBS emphasized that the results for the fourth quarter significantly missed market expectations, and margins fell to their lowest level in 10 years. The expert also noted that signals from the management board indicate further margin pressure in 2026.

In turn, according to Bloomberg Janusz Pięta from mBank assessed the results as clearly negative, pointing out that the deterioration in profitability was much deeper than expected by the market. The analyst drew attention to the fact that Dino fared significantly worse compared to its main competitor – Biedronka (Jeronimo Martins), which managed to improve its EBITDA margin on an annual basis during the same period.

Why is Dino losing profitability?

There are several reasons for such a sharp decline in margins. First of all, the company had to face the so-called shopping basket deflationwhich means that the prices of basic products in stores are falling year on year, despite the occurrence of food price inflation. Deflation appeared at the end of 2025. In the face of consumer caution and their increasing price sensitivityDino decided to aggressively “invest in prices” to maintain sales volumes and customer interest.

Jakub Viscardi from BOS Bank stated in his commentary that such a large gross margin erosion is a very weak signal. According to him, the company's strategy for 2026, which assumes prioritization of Like-for-Like (LFL) sales growth at the expense of profitability, raises justified concerns among investors. Growing labor costs and high investment outlays (CAPEX) turned out to be an additional burden on the results.which amounted to PLN 511 million in the fourth quarter.

The brokers' favorite fails

It is worth recalling that at the beginning of 2026, Dino Polska was one of the most favored stocks on the WSE. The company was included in the “top pick” lists of 5 out of 9 domestic brokerage houses. The market widely expected that 2026 would see a recovery in operating margins due to easing cost pressures. Investors hoped that further scaling of the network (the number of stores has already exceeded 3,000 outlets) will translate into better purchasing conditions from suppliers and thus a higher gross margin.

However, the reality turned out to be more complicated. In addition to internal operational challenges, such as the conflict between the management and the staff, which Katarzyna Wiązowska describes in Bankier.pl, the company must face external challenges related to consumer habits. Analysts point to a weakening of retail trends resulting from the increase in consumer wealth. A richer society begins to spend a relatively smaller part of its income on food, which affects the foundations of the growth of supermarket chains that build their businesses around basic necessities (so-called consumer staples).

The prospects are no dividend and high investments

The management's forecasts for the coming months did not reassure the market. The Management Board of Dino Polska adopted only a “moderately positive” scenario for 2026, admitting that deflation will remain an important factor affecting sales dynamics. As summarized by Janusz Pięta from mBank, LFL forecasts only indicate year-on-year growth, there is uncertainty as to the EBITDA marginand CAPEX forecasts are high and amount to PLN 2.5 billion compared to PLN 2.1 billion on the market. Additionally, the company suggested no dividend payment despite generating net cash.

The only real “consolation” in the report was strong cash flow and the fact that the company reports positive net cash. The market now needs to revise its expectations. Dino is no longer the favorite of foreign capital, which has fueled the company's share price for years, seeing how the company is growing. The expansion of the network is progressing because management forecasts indicate the opening of approximately 390 new stores – above our market expectations (371)but the erosion of margins that have impressed the company as a money-making machine for years are getting weaker, and the chain itself becomes a participant in a brutal price war on the saturated Polish market. If the scenario of rebuilding profitability in 2026 does not materialize, the premium with which Dino was previously valued on the WSE may be further reduced.