Exactly three years ago – on November 7, 2022 – WIBOR 3M reached the highest level in recent years. Since then, it has dropped from 7.61%. up to 4.3 percent (according to data published at the end of November 6, 2025), i.e. by 3.3 percentage points. This translates into lower interest rates on loans and deposits (in the case of loans, the bank's margin must be added).

– This is why in November 2022, the average interest rate on newly granted loans with variable interest rates exceeded 9.6%, according to NBP data. Now, when WIBOR is much lower, this rate has grounds to drop to around 6.3%. , that is, by almost one third, and this is probably still not the end – says analyst Bartosz Turek.

In three years, the situation has changed 180 degrees. We entered November 2022 after a record-breaking tightening of monetary policy (the reference rate increased from 0.1% to 6.75% during the year). If that were not enough, at the beginning of November the market was still expecting further interest rate increases, which pushed WIBOR rates up. Only after the second decision in a row to leave interest rates unchanged did economists' predictions begin to change.

|

Bartosz Turek

Now we are in a completely different place. This year, there has already been a series of cuts that brought the basic interest rate to 4.25%. Moreover, further monetary easing is still ahead of us, with a probability bordering on certain. A cut cannot be ruled out even at the December MPC meeting, although today economists believe that such moves are more likely to occur in 2026.

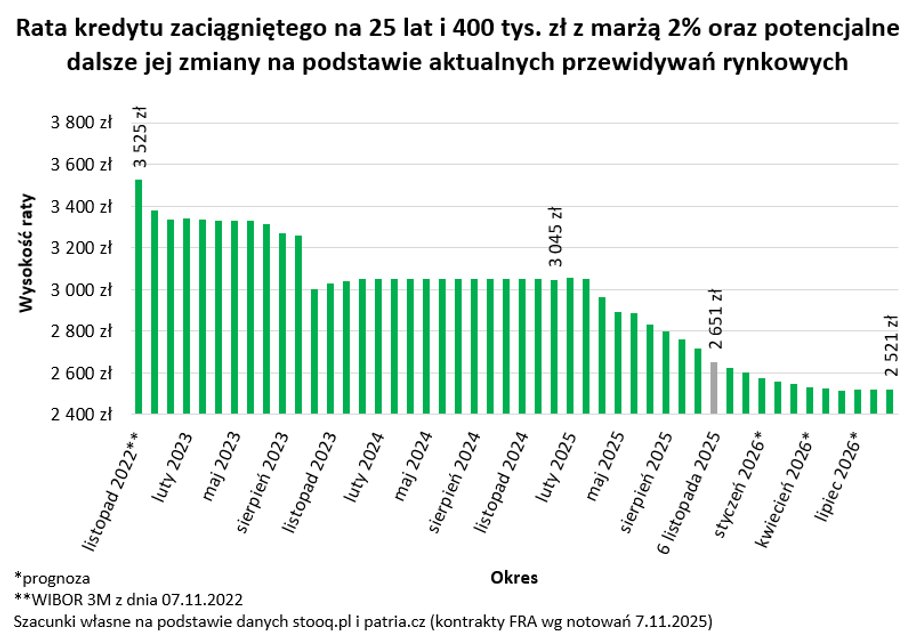

This is how installments are decreasing thanks to the reduction of rates by the Monetary Policy Council

What are the real consequences of the drop in interest rates? Bartosz Turek's calculations show that with a loan for 25 years and PLN 400,000. PLN, the monthly installment in November 2022 could exceed PLN 3,500. Now, when applying for such a loan, you should be prepared for an installment of approximately PLN 2,650. This means a decrease of one quarter

See also: “Banks will have no scruples.” This is how rate cuts will affect their results

A few words of explanation are necessary here. A basic question arises – why did the installment drop by 25% if the interest rate dropped by 1/3 or 1/3? The explanation here is the mechanism of the most popular fixed installments in Poland (not to be confused with a loan with a fixed interest rate). Equal installments system unlike decreasing installments In simple terms, it works by averaging the installment amount over the entire loan period: if the interest rate, and therefore the interest, is high, there is “little space” in the loan installment for the repayment of the principal. However, when the loan interest rate falls, the lower interest gives room to repay the capital faster. This is why in this loan repayment system the installments fall slower than the interest rate. We write more about the differences between equal and decreasing installment systems here.

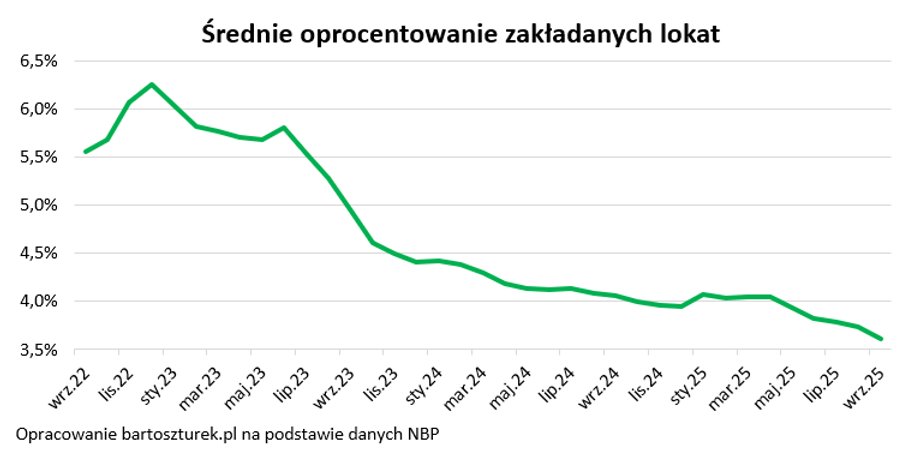

Deposit interest rates have already fallen by about half

Lower interest rates may please borrowers, but they worry savers. — At the end of 2022, the average bank deposit had an interest rate of over 6.3%. The latest NBP data are available for September 2025. Already then, the average interest rate on deposits actually opened had dropped to 3.6 percent. Now it is almost certainly lower, because in the meantime the Monetary Policy Council has reduced interest rates by a total of another 0.5 points. percent – says Bartosz Turek.

Taking into account available forecasts, the average interest rate on savings in banks may soon drop below 3%. This is important from the point of view of the housing market, because with such low interest rates, savers can look for more profitable ways to invest capital.

|

Bartosz Turek