publication

2026-03-30 22:05

The New York stock exchanges ended in negative territory for the third session in a row, and the Nasdaq and S&P500 deepened their over six-month lows. Investors did not like President Trump's belligerent attitude. It is worth noting, however, that treasury bonds rose in price despite rising oil prices.

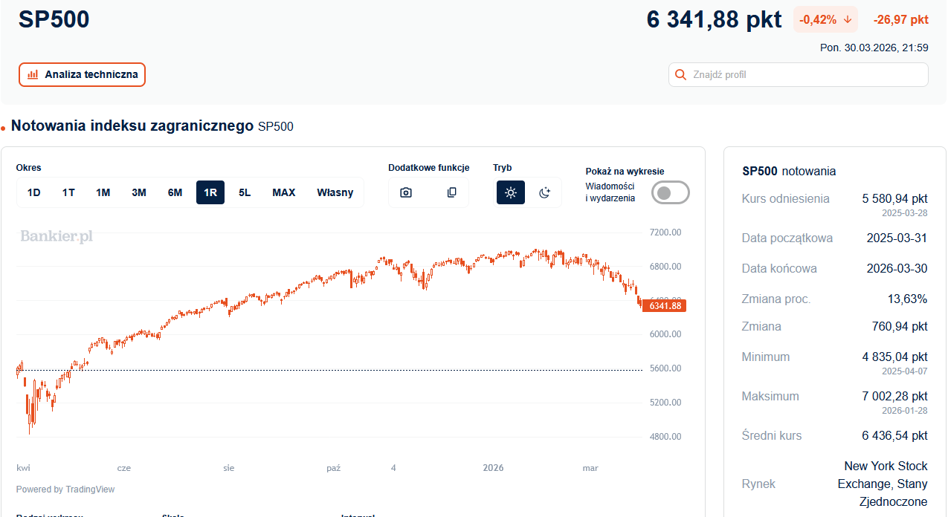

The S&P500 index ended lower for the third session in a row, this time losing 0.39% and falling to 6,343.72 points. In this way, the most important American stock benchmark deepened Iran's declines and reached the lowest level since August. Since the peak at the end of January, the S&P500 has already lost nearly 10% and is on the conventional border of correction.

The Nasdaq Coposite fell 0.73%, falling to 20,794.64 points. It was the third declining session in a row after the Nasdaq fell by more than 2% on Thursday and Friday. It has been 5 months since the index reached its last peak, from which it is now almost 14%. However, the Dow Jones industrial average managed to gain 0.11% and at the end of the session rebounded from the lowest level in 7 months.

Advertisement

As usual, the main culprit for the decline in March was the situation in the Middle East. The weekend brought an escalation of military operations and dismissed hopes for peace with Iran. The US president again threatened to destroy Iran's energy sector if Tehran does not bow to American demands. The Persians once again rejected the American conditions for cessation of hostilities.

“Great progress has been made, but if for some reason an agreement is not reached quickly, as it likely will be, and if the Strait of Hormuz is not opened for business immediately, we will end our lovely stay in Iran by blowing up and completely destroying all of their power plants, oil wells, and Khark Island (and maybe all of their desalination plants!) that we have not yet touched,” US President Donald Trump wrote.

So, on the one hand, the Americans are negotiating with a “more reasonable regime”, and on the other hand, they are threatening war crimes and the annihilation of one of the largest oil and gas producers. It is therefore hardly surprising that Brent crude oil prices increased by another 2.8%, reaching over USD 108 per barrel. This is still very expensive. This price level threatens to destroy economic growth and guarantees a strong increase in CPI inflation practically everywhere in the world.

In this context, it is worth noting that the debt market calmed down a bit on Monday. The yield on US 10-year bonds dropped by over 9 basis points, falling to 4.34%. On Friday, it reached almost 4.5% and was the highest since July. Two-year Treasuries offered 3.83% YTM, which is clearly less than over 4% before the weekend. This would suggest that the older and wiser debt market is pricing in future US inflation pressures slightly lower.

Bets that the Federal Reserve will raise interest rates this year have also weakened significantly. Today, the futures market estimated the chances of such a scenario to be realized at only 3.7%. And just a few days ago it was close to 50%. This was most likely the result of Jerome Powell's speech on Monday. The Fed chief said that monetary policymakers can wait to react to the effects of the war with Iran and that they usually do not raise interest rates in response to a supply shock. This was a quite clear hint that the Fed did not intend to tighten monetary policy any time soon. Such statements were intended to calm financial markets and “recalibrate” investor expectations.

Later in the stock market week, the markets' attention may shift towards the American labor market. On Tuesday, we will know the February number of unfilled vacancies according to: JOLTS surveys, on Wednesday the ADP report measuring changes in employment in the private sector, on Thursday the March Challenger Report (on the number of declared group layoffs in the corporate sector), and on Good Friday (day without a session on Wall Street) a monthly report on the unemployment rate and changes in employment in non-agricultural sectors will be published.

The publication contains affiliate links.