Polish industry is in decline, but there is light at the end of the tunnel. First important data in 2026

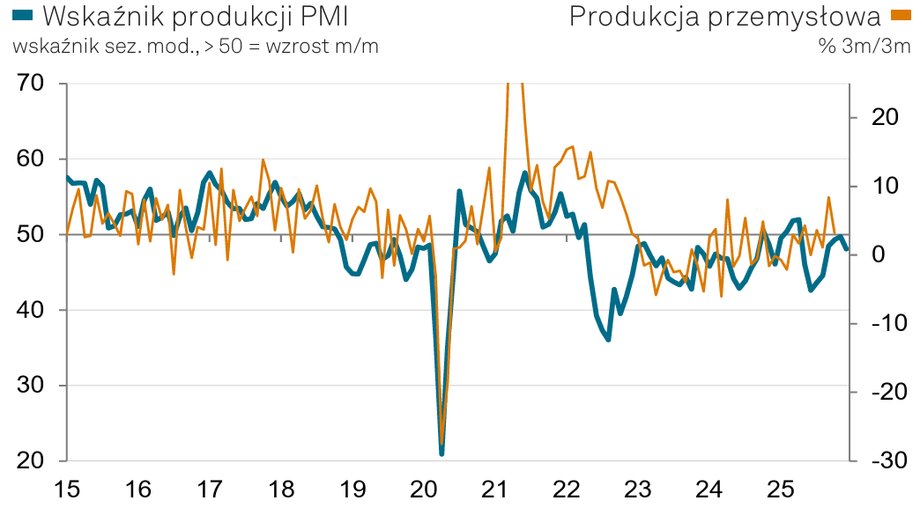

The PMI index for Polish industry in December 2025 was 48.5 points, which is down from 49.1 points a month earlier – S&P Global reported on Friday. This result is slightly worse than forecast, as the result was expected to be around 49 points. The December result was close to the average for all of 2025 of 48.3 (the highest since 2021).

A score of 50 points is an important barrier that separates expansion (readings above this limit) from recession (below) in the sector. Not only is it important whether it is below this cut-off level, but an important indication is whether a change is taking place: a rising PMI, even if it is below 50 points, suggests improvement in the sector. The index shows a high correlation with the dynamics of industrial production (data in this respect will be available on January 22).

More optimism among Polish companies

In December, the index for Polish industry was below the 50-point barrier for the eighth month in a row. This was the first monthly decline in the index since June, and the latest reading still showed only a moderate deterioration in industrial conditions. Faster declines in production and new orders were partially offset by slower declines in employment and inventories of purchased items, as well as longer delivery times.

New orders fell for the ninth time in a row in December, at the fastest rate in three months. Meanwhile, new export orders signaled a decline after an increase recorded in November. Some companies reported weak conditions in the German and French markets. The continued decline in new orders translated into lower production levels in December. The latest decline was the fastest in four months and extended the current downtrend to eight months, according to a report by S&P Global.

|

S&P Global

Although declines in new orders and production accelerated somewhat in December, Polish producers were much more optimistic about increasing production in the next 12 months than they were in November. The future production index signaled the second-biggest growth recorded over the past five years. Overall sentiment was the best since March 2025 and returned to levels close to the long-term average (since 2012). The survey respondents associated positive forecasts with the expected improvement in the market situation, company development projects and new customers.

Employment and supply indicators suggested that industrial capacity was largely in line with production requirements at the end of 2025. Employment fell for the eighth time in a row, although the pace of decline was moderate. Production backlogs decreased for the third time in a row, but only slightly, and the production backlog index recorded a value above the long-term trend.

Better second half of the year

“At first glance, the decline in PMI since November, in the face of stronger declines in production and new orders, painted a pessimistic picture of the industrial situation at the end of 2025. However, the entire second half of the year showed a clear upward trend, with PMI rising continuously between July and November, representing the longest sequence of increases since 2013.” – wrote Trevor Balchin, economic director at S&P Global Market Intelligence, in a comment.

“The Future Production Index provided further evidence that it is on the road to recovery as we enter 2026. The index recorded the second-largest monthly gain seen over the past five years, returning to the level of its long-term trend (since the index's inception in 2012). Additionally, the production backlog index was above its long-term trend,” he added.